Crosby's Per-Document Pricing: A Concrete Case Study in Inverting the Billable Hour

This article examines Crosby, an AI-native law firm that has abandoned the billable hour for fixed per-document pricing ($250–$1,000 per contract). For law firm partners, legal ops leaders, and industry analysts, it analyzes how this model structurally aligns firm incentives with client goals and what it signals for the future of legal services delivery.

Lex Machina Review is an independent risk-tracking and reference resource. Nothing on this site is legal advice, and using it does not create an attorney-client relationship. Every record is reviewed against primary sources but may not reflect the most current status of a matter — always verify directly against the cited court order, rule text, or a licensed attorney before relying on it.

Companion explanation — secondary to the source document above

The Billable Hour's $69 Billion Question

In 2024, the 100 highest-grossing law firms in the United States generated a combined $69 billion in net income. Every dollar of that sum was distributed to the firms' partners as compensation. That figure — drawn from Law.com data and cited by Crosby's own CEO — is larger than Google's annual R&D budget. It represents the financial apex of a billing model that has governed the legal profession for more than half a century.

The billable hour is not merely a pricing mechanism. It is an organizing principle that shapes how firms allocate talent, how associates are trained, how technology is adopted, and how value is perceived by clients. Every six-minute increment tracked by a timekeeping system encodes an incentive: more hours produce more revenue. That logic is so deeply embedded in law firm operations that most practitioners treat it as a natural law of the profession rather than a contingent business choice.

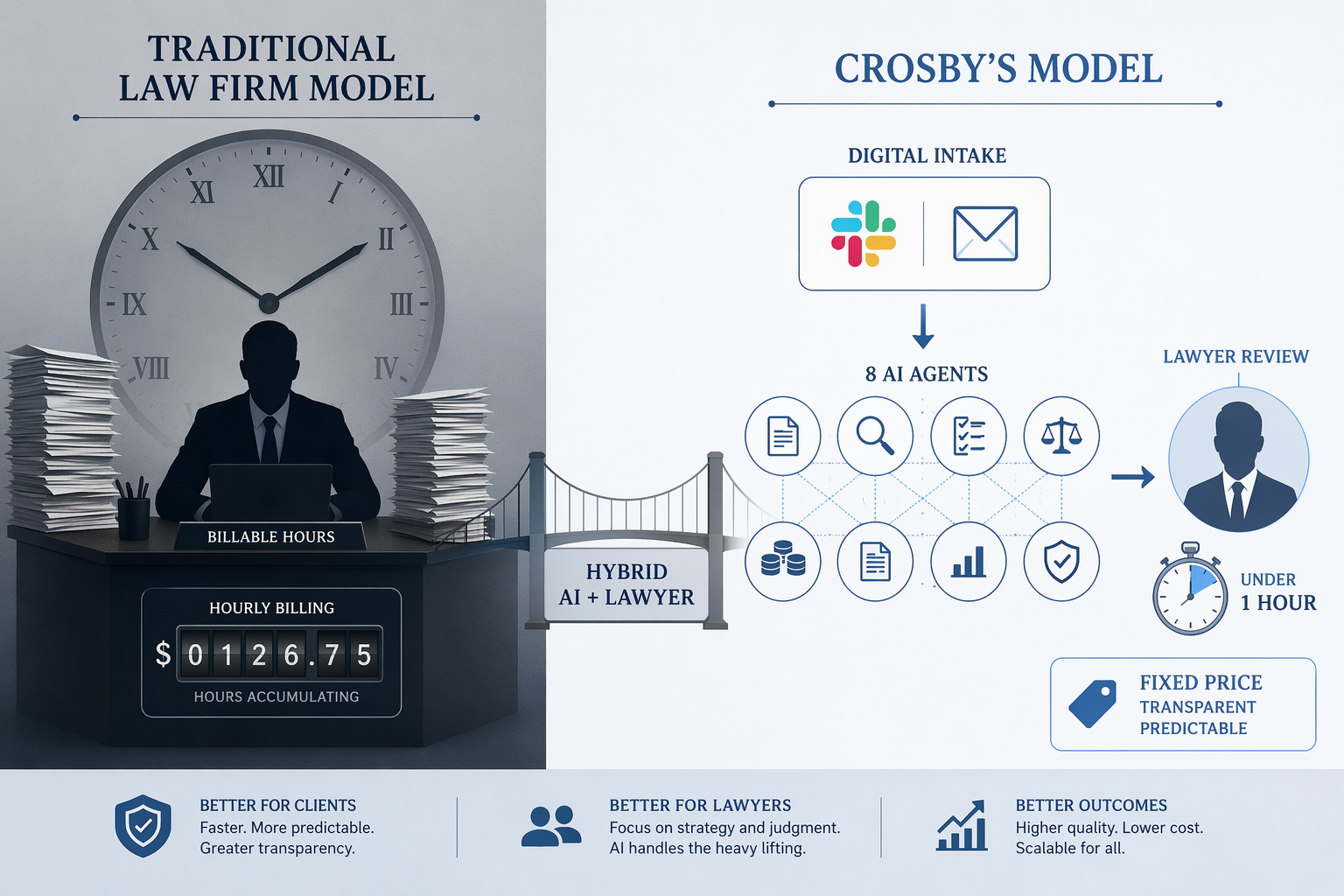

Crosby, an AI-native law firm that emerged from stealth in late 2025, has built its entire operating model around a different premise. The firm charges a fixed fee per contract — $250 to $1,000, or $10 to $50 per page — billed once regardless of how many rounds of negotiation a document requires. In doing so, it has inverted the fundamental incentive structure of legal services. Where a traditional firm profits by maximizing hours, Crosby profits by minimizing turnaround time. The faster and more accurately a contract is reviewed, the more contracts the firm can process, and the more revenue it generates. Client goals (speed, cost predictability) and firm goals (volume, deal velocity) are structurally aligned rather than structurally opposed.

How Crosby's Per-Document Pricing Works

Crosby's pricing is straightforward: a client submits a contract — an NDA, a SaaS agreement, an employment contract, a vendor services agreement — and receives a redlined version with proposed revisions. The cost is a flat fee per document, not a function of how many hours a lawyer spends on it. According to Forbes reporting from March 2026, the range is $250 to $1,000 per contract, or $10 to $50 per page. A contract that requires three rounds of negotiation costs the same as one that closes in a single pass.

The operational metrics that replace billable hours reveal the inversion clearly. Crosby tracks two primary numbers, as described in Sequoia Capital's Inference publication: TTAT (total turnaround time), the complete interval from contract receipt to final signature, and HuRT (human review time), the portion of that interval requiring direct lawyer attention. The firm's stated median turnaround is 58 minutes. By measuring and minimizing both metrics, Crosby creates a direct feedback loop between operational efficiency and revenue capacity.

| Metric | Traditional Firm | Crosby |

|---|---|---|

| Pricing unit | Hourly rate ($500–$1,000/hour) | Per document ($250–$1,000) |

| Revenue driver | Hours worked | Contracts processed |

| Incentive direction | Maximize time per matter | Minimize time per matter |

| Core metric | Billable hours | TTAT (total turnaround time) |

| Cost to client | Variable, unpredictable | Fixed, known upfront |

| Negotiation rounds | Each round adds billable time | Included in flat fee |

The results, at least in the early data, are striking. Cursor, the AI coding startup, has used Crosby for approximately 2,000 contracts and reports a 50% reduction in review time, according to Forbes. Crosby itself states that it has reviewed 13,000 contracts since inception, with revenue growing 400% between October 2025 and March 2026. The firm has negotiated $1 billion in aggregate contract value, up from $30 million at the time of its stealth exit 283 days prior, as reported by TAMradar.

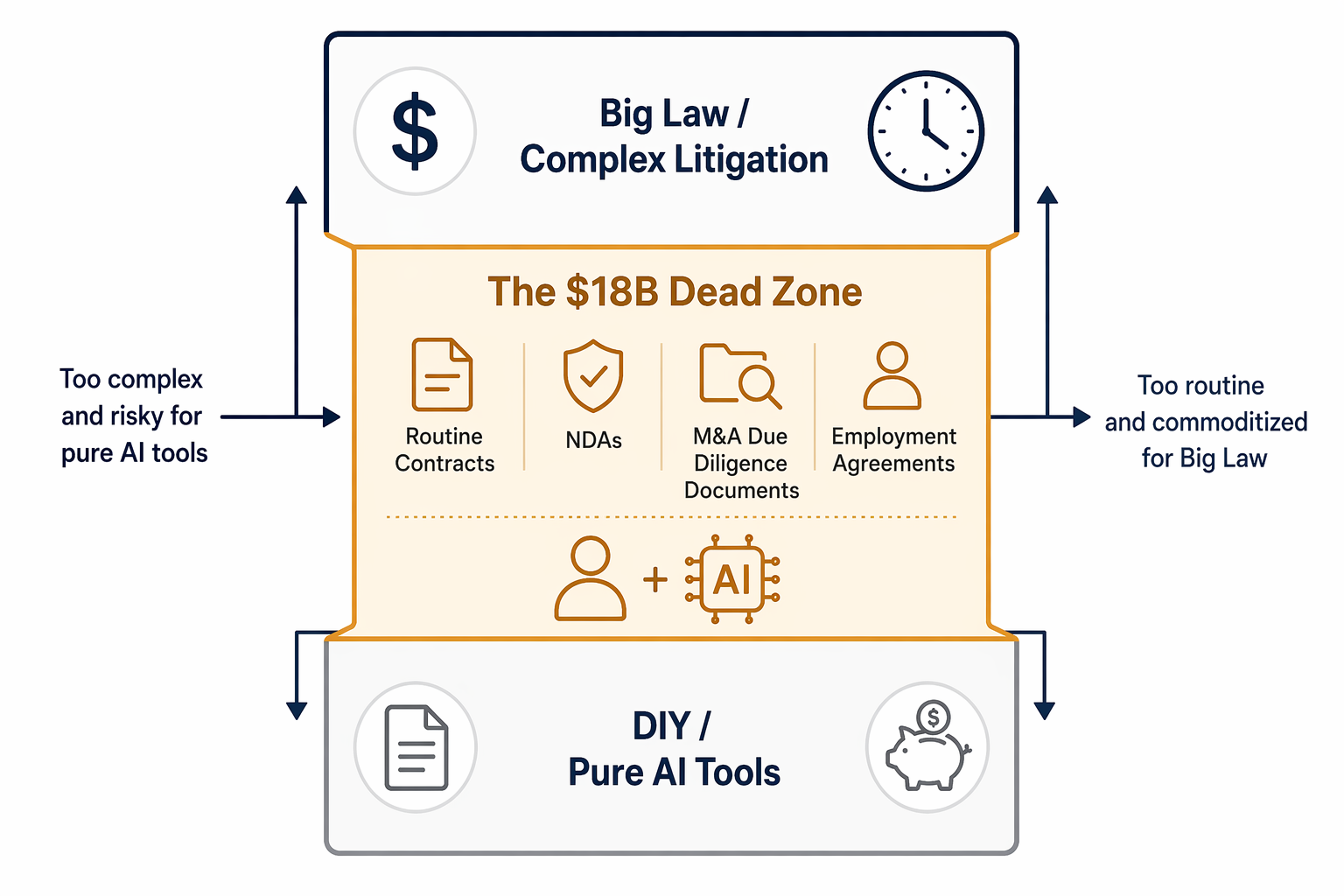

The $18 Billion 'Dead Zone' Thesis

Crosby's market positioning rests on what its investors at Bain Capital Ventures call the "dead zone" thesis: a segment of legal work that is too complex for pure AI tools to handle autonomously but too routine to justify Big Law billing rates. BCV quantifies this market at $18 billion, drawn from the legal process outsourcing market size. It encompasses the contracts that every company generates in volume — NDAs, vendor agreements, employment terms, SaaS subscriptions, partnership agreements — that require legal judgment but do not demand the full apparatus of a law firm partnership.

This segment is structurally underserved by both ends of the market. Traditional firms apply their standard hourly rates to this work, which makes clients reluctant to engage them for anything but the most critical documents. Pure AI tools, meanwhile, lack the legal judgment to handle nuanced provisions — the Sequoia publication notes that phrases like "commercially reasonable" versus "reasonable" look identical in embedding space but carry vastly different legal implications. A general-purpose LLM cannot reliably distinguish them without human supervision.

Crosby's hybrid model — AI agents performing initial review and drafting, with licensed attorneys providing final judgment — fills this gap. The firm positions itself as a vertically integrated alternative to both the law firm and the software vendor. It takes liability for its work, carries malpractice insurance, and is registered as a law firm. But it operates at a cost structure and speed that no traditional firm can match for this type of work.

Crosby as a 'Neofirm': Building Services as Software

Crosby's operational model is distinct from both traditional law firms and AI software companies. The firm employs eight specialized AI agents built on top of models from OpenAI, Anthropic, and Gemini, each trained for specific contract review tasks. Lawyers sit alongside engineers in the same workspace, creating what the firm describes as tight feedback loops between legal judgment and model refinement. This structure, detailed in Upstarts Media's reporting on Crosby's Series A, allows the firm to treat every contract review as both a client service and a training data point.

The network effect is central to Crosby's thesis. As the BCV blog post explains, contract clauses function like code in Crosby's system. Each review adds to a living dataset of clauses, redlines, and outcomes. The more contracts the firm processes, the more its AI agents learn about how specific provisions are negotiated in practice. This creates a compounding advantage that pure software tools cannot replicate, because the data comes from real negotiations with real outcomes, not from training corpora.

- Eight specialized AI agents handle initial review, clause extraction, and redlining, each optimized for specific contract types and provisions.

- Licensed attorneys review every output before it reaches the client, providing the legal judgment that AI cannot yet reliably deliver.

- Engineers and lawyers work in alternating seating arrangements, enabling real-time model adjustments based on attorney feedback.

- Every contract review generates structured data that improves the system for future reviews, creating a compounding dataset.

- The firm is a registered law entity with malpractice insurance, not a software-as-a-service product — clients receive legal services, not software outputs.

This "neofirm" category — a vertically integrated legal services provider that combines AI automation with licensed attorney judgment under a single business entity — is distinct from the AI assistant tools (Harvey, CoCounsel) that augment existing law firms, and from the pure platforms (Ironclad, Kira) that provide software without legal representation. Crosby does not sell software licenses. It sells legal outcomes, priced per document, with the firm bearing the professional liability.

What This Means for Law Firm Profitability, Associate Development, and Client Value

Crosby's model has implications that extend well beyond its own market share. For law firm partners evaluating their own business models, three dimensions deserve attention.

Profitability Models: R&D Investment vs. Partner Distributions

The $69 billion in AmLaw 100 net income in 2024 was distributed entirely to partners. Crosby's CEO Ryan Daniels has explicitly contrasted this with his firm's approach: Crosby reinvests profits into technical R&D, model training, and infrastructure rather than distributing them as compensation. This is not a moral argument — it is a structural one. A firm that reinvests its margins into improving its production system can compound its capabilities over time. A firm that distributes its margins cannot. For legal ops leaders evaluating long-term vendor relationships, this distinction matters: a neofirm that improves with every engagement offers a different trajectory than a traditional firm that maintains the same cost structure year over year.

Associate Development: What Junior Lawyers Learn

Traditional law firm training relies on the apprenticeship model: junior associates learn by reviewing documents under senior supervision, gradually building pattern recognition through repetition. Crosby's model automates much of that repetition. The question this raises — and that the legal industry has not yet answered — is what happens to the training pipeline when AI handles the routine work that historically built foundational legal judgment. Crosby's lawyers focus on the edge cases and nuanced provisions that the AI agents flag, which may produce stronger training for the lawyers who remain. But the model employs far fewer lawyers per volume of work than a traditional firm, which changes the scale and nature of the training environment.

Client Value Perception: Predictability as a Product

For clients — particularly startups, mid-market companies, and in-house legal teams — the most immediate benefit of Crosby's model is predictability. A fixed per-document price means legal costs are known before work begins. There is no surprise invoice for an extra round of negotiation, no internal debate about whether to engage outside counsel for a routine NDA. The BCV blog post frames this as turning legal from a variable expense into a reliable operating function. For legal ops leaders managing budgets across multiple departments, this predictability has real value that the billable hour cannot offer.

The Limits of the Model: Sophisticated Work and the Billable Hour's Staying Power

Harvard Law professor Robert Couture, quoted in the Forbes article on Crosby, offers a necessary counterpoint: the billable hour is not disappearing for sophisticated, bespoke legal work. Complex litigation, multi-jurisdictional mergers, regulatory investigations, and bet-the-company transactions require a level of customization and strategic judgment that does not fit a per-document pricing model. The billable hour survives in these contexts because it is, for all its flaws, a reasonable proxy for the value of highly specialized, non-replicable expertise.

Crosby's leadership does not dispute this. The firm's stated target market is the $18 billion "dead zone," not the $1.1 trillion global legal services market in its entirety. The firm processes contracts — it does not litigate cases, structure complex transactions, or provide regulatory counsel. The question is not whether Crosby's model replaces Big Law, but whether it demonstrates that the billable hour is no longer the only viable organizing principle for legal services, even within a defined segment.

The answer appears to be yes. Crosby's revenue growth — 400% in five months — and its ability to attract blue-chip venture investors (Index Ventures, Lux Capital, Sequoia, Bain Capital Ventures) suggest that the market for per-document legal services is real and growing. The firm's $60 million Series B at a $400 million valuation, announced in the same week as Harvey's $200 million round at an $11 billion valuation, signals that investors see multiple viable models in the legal AI space, not a single winner-take-all outcome.

Competitive Context: The Neofirm Landscape in 2026

Crosby is not alone in building a new category of legal services delivery. The first half of 2026 has seen a wave of funding for firms that combine AI with licensed legal practice. The table below summarizes the major players as of June 2026, based on publicly reported funding rounds.

| Company | Latest Round | Amount Raised | Valuation | Category |

|---|---|---|---|---|

| Harvey | Series D (Mar 2026) | $200M | $11B | AI Assistant for Law Firms |

| Crosby | Series B (Mar 2026) | $60M | $400M | Neofirm (Hybrid AI+Lawyer) |

| Eudia | Series A (2025–2026) | $105M | Not disclosed | Neofirm |

| Lawhive | Series B (Feb 2026) | $60M | Not disclosed | Neofirm |

| Manifest | Series A (2025–2026) | $60M | Not disclosed | Neofirm |

| Ivo | Series A (2025–2026) | $55M | Not disclosed | Neofirm |

Related records

Tool profile

Browse tool evaluations →Governing regulation

Browse the obligations tracker →Preventive workflow

Browse verification workflows →

Report a correction or tip

Spotted an outdated figure, a misstated fact, or a ruling this case record should reflect? Public comments are disabled for this content given the professional cost of a misreported case outcome, penalty amount, or rule text — use the structured correction channel instead.

Report a correction or tip for this record →