The 2027 Social Security COLA is currently being discussed in a range that is large enough to matter before it is official. The Senior Citizens League has projected a 3.8% adjustment, while independent analyst Mary Johnson has projected 4.7%; the official figure will not be announced until October 2026 and will depend on the applicable CPI-W measurement period.[1][2] For tax lawyers and planners, the useful question is not whether the final number lands at the low or high end. It is whether any increase in that range pushes a client’s provisional income across the same dollar thresholds Congress wrote into IRC §86 in 1983.

At the 3.8% estimate, the average retired-worker benefit would rise from about $2,026 per month to about $2,103 per month, or roughly $77 more per month.[1] That looks modest until it is placed inside the federal tax formula. A single retiree receiving that average benefit would have annual Social Security benefits of roughly $25,236 before considering any pension, IRA distribution, bank interest, part-time earnings, or tax-exempt interest. Because §86 counts one-half of Social Security benefits in provisional income, that COLA does not merely increase cash flow; it increases one component of the tax trigger.

The tax problem starts with provisional income, not the COLA headline

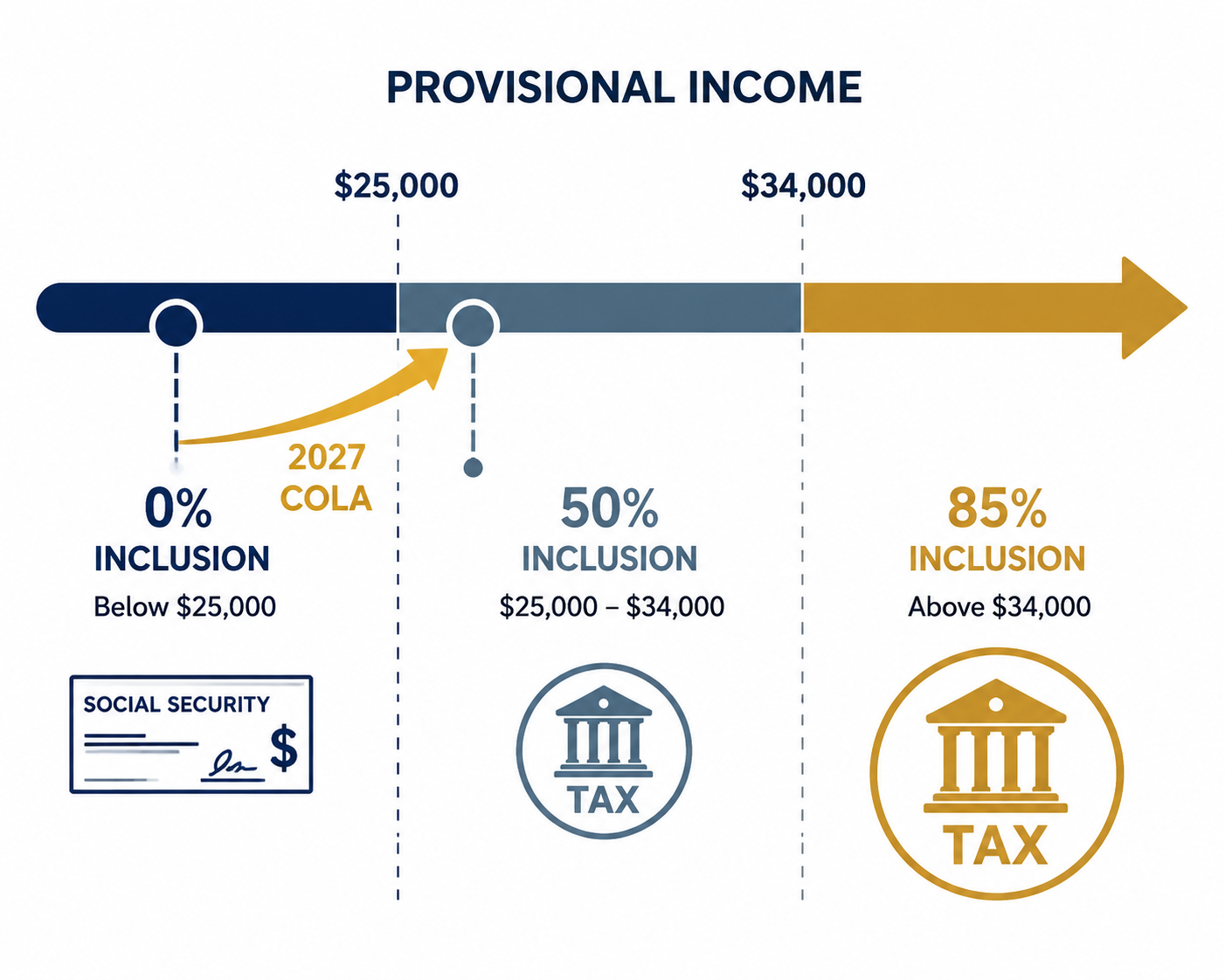

IRC §86 does not tax Social Security benefits merely because a retiree receives a larger monthly check. It taxes benefits by comparing the taxpayer’s provisional income to statutory base amounts. Provisional income generally means adjusted gross income, plus tax-exempt interest, plus one-half of Social Security benefits, with modifications set out in the statute.[3] That formula is why a benefit increase can change the tax result even when the retiree’s pension, IRA withdrawal, municipal bond interest, or wages do not change at all.

For single filers, the first relevant threshold is $25,000 and the second is $34,000. For married taxpayers filing jointly, the corresponding thresholds are $32,000 and $44,000.[3] Between the lower and upper thresholds, up to 50% of benefits may be included in gross income. Above the upper threshold, up to 85% may be included.[3] These are inclusion ceilings, not flat taxes on the entire benefit, but they are still the mechanical reason a nominal COLA can produce a larger taxable benefit.

| Filing status | Provisional income range | Potential federal inclusion of Social Security benefits |

|---|---|---|

| Single | At or below $25,000 | No taxable benefits under the basic §86 threshold structure |

| Single | Over $25,000 and up to $34,000 | Up to 50% inclusion |

| Single | Over $34,000 | Up to 85% inclusion |

| Married filing jointly | At or below $32,000 | No taxable benefits under the basic §86 threshold structure |

| Married filing jointly | Over $32,000 and up to $44,000 | Up to 50% inclusion |

| Married filing jointly | Over $44,000 | Up to 85% inclusion |

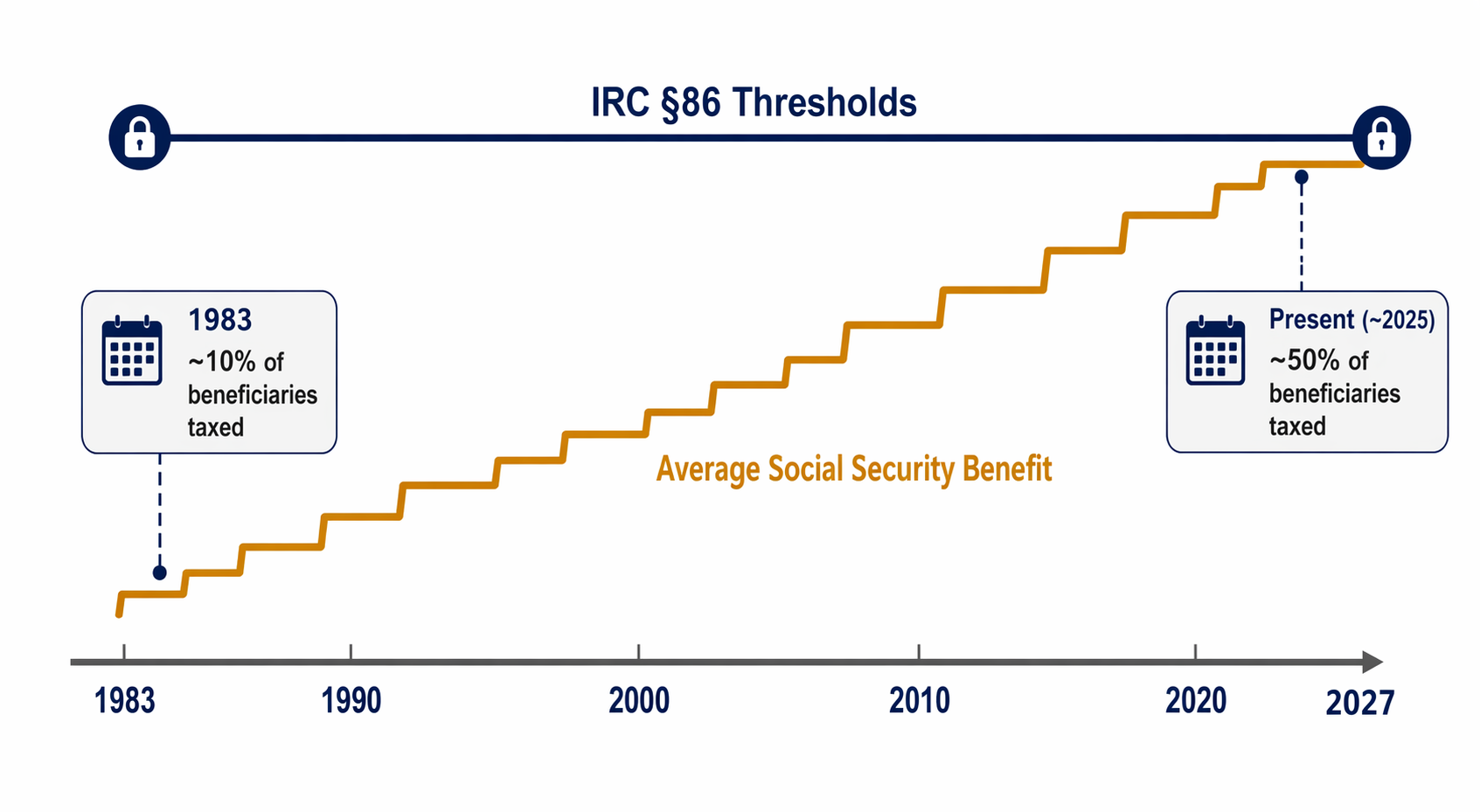

The thresholds are the legal sore point. They have not been indexed for inflation since enactment in 1983. The Congressional Research Service reports that about 10% of Social Security recipients paid federal income tax on their benefits when taxation began, compared with roughly half of recipients today.[4] That change did not require Congress to lower the thresholds. Benefit growth, outside income, and inflation did much of the work against fixed statutory amounts.

How a modest benefit increase becomes taxable income

Consider the common client profile rather than an extreme one: a single retiree with Social Security, a small pension, periodic IRA withdrawals, and a savings account that finally earns visible interest. The COLA raises the annual benefit. One-half of that increase enters provisional income. If the client was already near $25,000, the increase can move part of the benefit into the 50% inclusion zone. If the client was near $34,000, it can increase exposure to the 85% inclusion calculation.

That result often feels irrational to clients because the monthly increase was described as inflation relief. Legally, though, there is no contradiction. The COLA raises benefits under the Social Security program. Section 86 then aggregates those benefits with other income under a separate income tax rule. The tax law does not ask whether the retiree feels better off after groceries, insurance, utilities, and local taxes. It asks whether provisional income exceeds fixed statutory numbers.

The effect is especially easy to miss in client conversations because the marginal change is split across forms and months. The Social Security notice shows a larger benefit. The custodian reports the IRA distribution. The bank reports interest. The return-preparation software performs the §86 calculation months later. By then, the client remembers the COLA as a raise and experiences the return as a surprise.

The low-end forecast is already enough to model

There is no need to pretend that a 3.8% forecast is final in order to use it. Forecasts based on partial CPI-W data can move before the October 2026 announcement.[1][2] But for planning purposes, the low end of the current range is a defensible stress point: if a client crosses a §86 threshold at 3.8%, the file deserves attention now. If the client crosses only at the higher estimate, the advice can be framed as contingent.

That distinction matters professionally. A forecast should not be sold to clients as settled law or as a guaranteed benefit amount. It can, however, be used to identify returns where the tax result is sensitive to a small increase in one-half of annual Social Security benefits. The legal issue is not prediction accuracy to the dollar; it is threshold proximity.

What attorneys should look for before the October announcement

The most useful review is not a broad retirement-income lecture. It is a file-level scan for clients whose 2025 or projected 2026 provisional income sits close to $25,000, $34,000, $32,000, or $44,000. Those are the clients most likely to experience the 2027 COLA as a tax change rather than only as a benefit increase.

- Recalculate provisional income using the client’s current Social Security benefit and then again using 3.8% and 4.7% benefit increases.

- Separate clients who cross the lower threshold from those who cross the upper threshold; the advice and client reaction will differ.

- Check whether IRA distributions, pension income, annuity payments, taxable brokerage income, or tax-exempt interest are doing more work than the COLA itself.

- Review withholding and estimated tax payment assumptions before the client receives an underpayment surprise.

- Flag estate and trust plans that assume a surviving spouse will remain in the same tax posture; the single-filer thresholds are materially lower than the joint thresholds.

The surviving-spouse point deserves particular care. A married couple may be comfortably under or modestly over the joint thresholds while both spouses are alive. After the first death, the survivor may have reduced household benefits but also a lower filing threshold, a compressed standard deduction posture, and many of the same account-level income sources. The 2027 COLA is not the only cause of that shift, but it can be the increment that exposes the problem in the first return after a death.

For clients near the line, timing choices may be worth modeling rather than prescribing reflexively. A Roth conversion, a larger IRA withdrawal, capital gain realization, or municipal bond allocation can all affect provisional income or later taxable income in different ways. The right answer depends on the client’s full tax map, not on the existence of a COLA. Still, the COLA forecast tells counsel which files deserve that map before year-end decisions harden.

The senior deduction may soften the bill, but it does not amend §86

The temporary $6,000 senior deduction under OBBBA is relevant, but it should not be confused with a change to the Social Security benefit inclusion rules. The deduction applies for 2025 through 2028 and phases out above $75,000 of MAGI for single filers and $150,000 for joint filers.[5] For eligible taxpayers, it may reduce taxable income and, in turn, tax due. It does not index the §86 thresholds, remove Social Security from provisional income, or prevent a COLA from increasing the amount of benefits included in gross income.

That is the distinction clients are least likely to hear in public descriptions of the deduction. A deduction can improve the bottom line on a return while leaving the underlying inclusion calculation intact. If the deduction later expires as scheduled after 2028, or if a client phases out of it, the §86 exposure remains waiting underneath. Planners should therefore model both layers: first, how much of the benefit becomes taxable under §86; second, whether any temporary deduction reduces the resulting taxable income.

State taxes are a secondary, but not imaginary, complication

Federal law is the center of the 2027 COLA issue because §86 supplies the frozen thresholds and inclusion formula. State treatment can still change the client’s actual result. Some states exclude Social Security benefits; others tax some benefits or apply their own income limits, deductions, or exemptions. A federal projection that stops at Form 1040 can therefore understate or overstate the cash-flow effect depending on the client’s residence and filing facts.

The state analysis should not be allowed to obscure the federal trigger. If a client crosses the federal provisional income threshold, that is a real tax event even if the state is generous. If the state also taxes some portion of benefits or uses income-sensitive relief, the same COLA can produce a second layer of analysis. The practical move is to identify the federal crossing first and then test the state overlay.

Buying power and taxable income are moving on different tracks

The Senior Citizens League has reported that Social Security benefits have lost 13.7% of buying power since 2010 even with COLAs.[6] That point should make practitioners cautious about describing the 2027 adjustment as a simple gain. A COLA can be necessary to help a retiree keep pace with prices and still increase the portion of benefits pulled into taxable income. Both things can be true because purchasing power and §86 inclusion are measuring different questions.

This is also why the legal implication of the 2027 forecast is broader than the official percentage. The exact COLA will matter for benefit notices, withholding, budgeting, and final projections. The structural issue is already visible: benefits are adjusted, while the statutory thresholds that determine taxation are not. Each year that pattern continues, more modest-income retirees with ordinary additional income become candidates for partial benefit taxation.

The professional takeaway

The 2027 Social Security COLA forecast should be treated as an early warning, not a final number. The prudent work before October 2026 is to model the current forecast range against the frozen §86 thresholds, identify clients near the lower and upper provisional income lines, and explain that a higher monthly benefit may also increase taxable benefits. If the client is close enough that a 3.8% COLA changes the result, the file is already in the risk zone; if the result changes only under the higher estimate, the advice can say so. The temporary senior deduction may reduce the pain for some taxpayers, but it does not repair the statutory mechanism causing the exposure.

References

- COLA Watch, The Senior Citizens League, 2026.

- Social Security cost-of-living adjustment could be highest since 2023, CNBC, June 12, 2026.

- 26 U.S. Code § 86 - Social security and tier 1 railroad retirement benefits, Cornell Legal Information Institute.

- Social Security: Taxation of Benefits, Congressional Research Service, CRS Report RL32552.

- One Big Beautiful Bill Act, Congress.gov, 2025.

- 2026 Loss of Buying Power Report, The Senior Citizens League, 2026.

Comments

Join the discussion with an anonymous comment.