The June 9, 2026 Social Security Trustees Report turned a familiar warning into a dated planning problem. The Old-Age and Survivors Insurance trust fund is now projected to be depleted in Q4 2032, with incoming revenue sufficient to pay 78% of scheduled benefits afterward. In practical terms, that is a 22% automatic benefit cut affecting 63 million current beneficiaries if Congress does not act before then. The combined OASDI trust funds are projected to reach depletion in Q3 2034, with a 17% cut at that point under the same no-action assumption. [1]

For lawyers advising retirees, disabled workers, surviving spouses, adult children, and fiduciaries, the question is not simply whether artificial intelligence can forecast Social Security benefit cuts. The sharper question is how benefit-cut projections, legal consequences, and AI forecasting fit together when the law already tells us something severe: a beneficiary's monthly payment is politically important, economically essential, and often morally treated as earned, but it is not an accrued property right that a court can preserve against statutory change.

The Legal Baseline Comes Before the Forecast

The controlling legal point remains Flemming v. Nestor. In that 1960 decision, the Supreme Court rejected the argument that paying FICA taxes creates a contractual or accrued property right to future Social Security benefits. Congress retained authority to alter, amend, or repeal benefit provisions, and the statutory scheme did not give beneficiaries the kind of vested entitlement that would prevent Congress from changing eligibility or payment rules. [2]

That doctrine matters because trust fund depletion is not just a budget forecast. The Antideficiency Act bars federal officers from obligating or spending beyond available appropriations and funds. CRS's legal analysis explains that, once trust fund reserves are insufficient, the Social Security Administration could not simply continue paying full scheduled benefits without legal authority and financing. Absent congressional action, payable benefits fall to the level supported by incoming revenue; the reduction is legally self-executing. [2]

This is the hard floor beneath every client conversation. A forecast can estimate the size of a household's exposure. It can model legislative alternatives. It can help counsel decide which documents, elections, and contingencies deserve review first. It cannot convert scheduled benefits into guaranteed property, and it cannot authorize SSA to spend money Congress has not provided.

Why the Cut Lands Differently Across Client Files

A 22% reduction is easy to flatten into an average. Lawyers cannot work with it that way. Rutgers Law has reported that 52% to 56% of beneficiaries derive at least half of their income from Social Security, and that one quarter of recipients derive at least 90% of their income from it. The same Rutgers discussion notes that Black and Latino recipients face roughly double the poverty rate of white recipients. [3]

Those numbers change the counseling posture. In an estate-planning file, the issue may be whether a surviving spouse can maintain housing costs after a reduction. In an elder-law file, it may be Medicaid planning, family contribution expectations, or the durability of a care arrangement. In a disability practice, the concern may be whether a benefit reduction destabilizes rent, transportation, or medication routines. The same percentage cut can be manageable for one household and catastrophic for another.

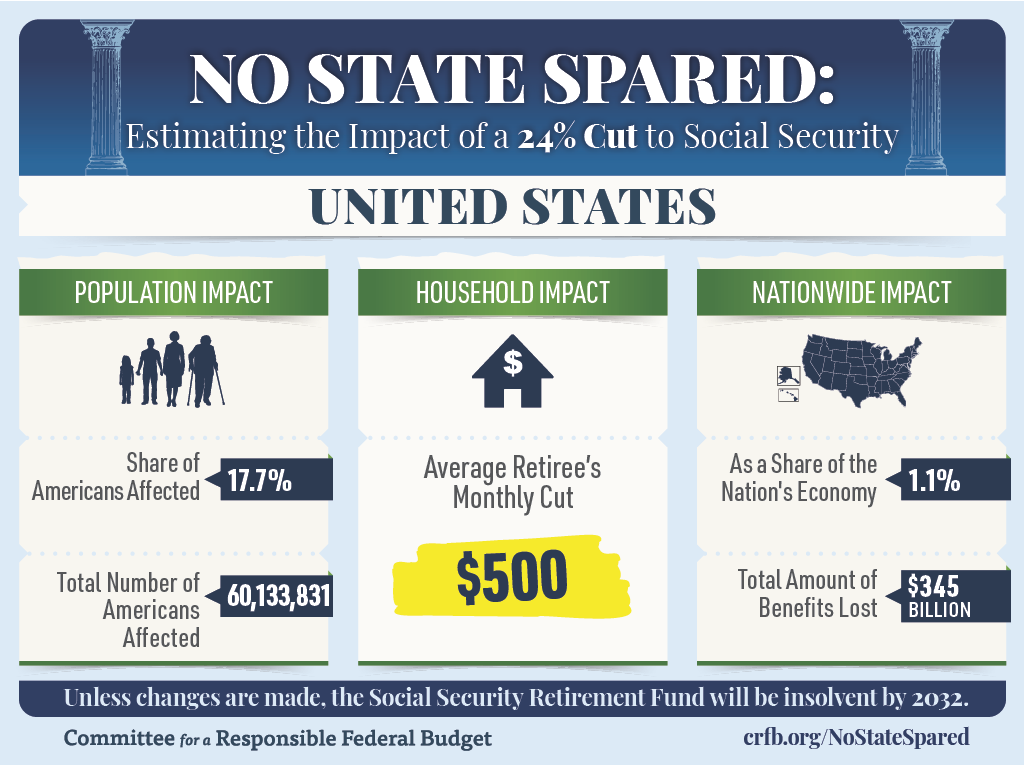

Geography adds another layer. The Committee for a Responsible Federal Budget's state-level mapping estimates an average national monthly cut of about $500 under insolvency, with projected average monthly reductions exceeding $550 in Connecticut, New Jersey, and New Hampshire. [4]

The map is useful not because state borders determine federal benefit law, but because cost structures and benefit amounts shape the client impact. A lawyer with clients in a high-rent state may need different assumptions than a lawyer advising a similar benefit recipient elsewhere. Forecasting that ignores that difference produces tidy numbers and weak advice.

Where AI Forecasting Can Help a Lawyer Ask Better Questions

The strongest use of AI here is not a single prediction that Congress will or will not act. It is structured scenario work. A law office can use forecasting tools to organize the variables that already belong in the file: client age, claiming status, household reliance on benefits, survivor exposure, state cost assumptions, health constraints, employment capacity, estate liquidity, and the timing of any legal elections that cannot be easily undone.

| Forecasting task | What the lawyer should use it for | What it must not imply |

|---|---|---|

| Baseline benefit exposure | Estimate the dollar effect of a 22% payable-benefit reduction on the client's household budget | That the scheduled benefit is legally guaranteed |

| Congressional scenario modeling | Compare possible reform paths, delayed action, partial fixes, or no-action outcomes | That a model can bind Congress or predict legislation with court-tested certainty |

| State-level impact comparison | Identify where projected monthly reductions and local costs create higher planning pressure | That federal benefit law varies by state |

| Claiming behavior review | Flag clients considering early claiming because of fear rather than individualized analysis | That early claiming is categorically right or wrong |

| Assumption documentation | Record what dates, cut percentages, income sources, and legal constraints informed the advice | That the forecast is a legal opinion on future congressional action |

This kind of workflow has value before it has perfect predictive power. It makes the lawyer separate facts that are fixed for now, such as the Trustees Report's projected depletion date, from facts that are contingent, such as whether Congress changes revenue, benefits, eligibility, taxation, or trust fund financing before Q4 2032.

It also makes fear visible. CNBC reported in March 2026 that 44% of non-retirees said they planned to claim Social Security early because they feared benefit cuts. [5] That is not proof that early claiming is the wrong choice for those individuals. It is proof that lawyers and financial professionals will see more clients treating a policy forecast as a trigger for an irreversible claiming decision.

A responsible AI-assisted intake could flag that situation without deciding it. If a client says the planned filing date moved up solely because of insolvency headlines, the file should show that counsel discussed the legal uncertainty, the benefit-reduction projection, the client's health and work assumptions, survivor implications, and the possibility of congressional action. The tool's job is to keep the questions from being missed.

A Practical Forecasting File

In a benefits or elder-law practice, an AI-supported Social Security planning file should be built around assumptions that can be reviewed later. The first assumption is the legal baseline: scheduled benefits may exceed payable benefits after trust fund depletion. The second is the current projection: OASI depletion in Q4 2032 and a 22% cut under the 2026 Trustees Report. The third is client-specific reliance: how much of the household budget depends on benefits, and who is harmed first if the payment drops.

From there, the model can run alternatives. One scenario assumes no congressional action before depletion. Another assumes a delayed partial fix. Another assumes a package that changes scheduled benefits or revenue before the cut date. The lawyer does not need to pretend each scenario is equally likely. In fact, ranking assumptions is one reason to use the tool. But every output should remain labeled as a scenario, not a promise.

The better systems will preserve source dates. That matters because older analyses may use different cut estimates. CRFB, for example, has used a 24% figure in earlier insolvency discussions, while the June 2026 Trustees Report figure in the current news cycle is 22% for OASI after Q4 2032. [1][4] Treating that discrepancy as a source-date issue is more useful than treating it as a debate to be won. The lawyer needs to know which assumption was used when the client made the decision.

The Accuracy Claim Needs a Fence Around It

Predictive analytics already has a place in legal practice, but the strongest reported accuracy claims come from narrower domains. ABA commentary in 2024 described AI predictive analytics in litigation as drawing on historical case data, judicial behavior, court tendencies, and similar litigation patterns. [6] NexLaw's 2026 discussion of legal predictive analytics describes reported accuracy levels in the 82% to 92% range for areas such as contract and employment case outcomes. [7]

Those figures should not be casually imported into Social Security policy forecasting. Litigation prediction often works from recurring case types, known forums, historical judges, pleadings, motions, and outcomes. Social Security reform forecasting depends on legislative bargaining, macroeconomic assumptions, election results, public pressure, trust fund accounting, and congressional timing. The data structure is different, and the validation record is not the same.

That does not make AI useless. It means the useful claim is narrower. A tool may be very good at organizing known inputs, comparing scenarios, detecting inconsistent assumptions, summarizing legislative proposals, or estimating the client-level dollar effect of a stated cut. It should not be described to a client as 92% accurate at predicting what Congress will do unless that specific claim has been independently validated for that specific task.

Legal Limits the Forecast Cannot Move

The most dangerous misuse of AI forecasting in this setting would be emotional laundering: taking a frightening legal reality, passing it through a polished model, and returning a comforting chart that sounds more certain than the law permits. The legal limits are not fine print. They define the advice.

- No property-right workaround: Under Flemming v. Nestor, FICA contributions do not create a contractual right to future scheduled benefits. [2]

- No spending workaround: The Antideficiency Act prevents SSA from paying full scheduled benefits if legally available funds are insufficient. [2]

- No permanent guarantee workaround: CRS has explained that even a congressional benefit guarantee would likely face limits because one Congress generally cannot bind a future Congress on Social Security benefit changes. [2]

- No forecasting workaround: A model can estimate the effect of a cut or reform, but it cannot create entitlement, prevent reduction, or supply appropriations.

This is where lawyers have to be more precise than public commentary. A client may say, "I paid in, so they cannot cut me." The legally accurate answer is uncomfortable: paying in matters politically and morally, but the Supreme Court did not treat it as a contract securing an unchangeable future benefit. A client may say, "The government would never let checks fall." That may be a political prediction; it is not a legal guarantee.

AI can help counsel show the difference. One column can display scheduled benefits under current law. Another can display payable benefits after projected depletion. A third can display a legislative-reform scenario. A fourth can identify assumptions that are not legal facts. The visual distinction matters because clients often hear all future numbers as promises unless counsel labels them otherwise.

Ethical Use Looks More Like Documentation Than Prediction

For a lawyer, the professional use of AI forecasting starts with competence and confidentiality. A tool that requires sensitive financial, medical, disability, family, or survivor information cannot be treated like a casual calculator. Counsel needs to understand what data is entered, where it is stored, whether it is used to train models, who can access it, and how outputs are generated. If the lawyer cannot explain the tool's role in the advice, the tool is doing too much.

The file should also distinguish legal advice from financial projection. A lawyer may advise that, under current legal analysis, benefit reductions after trust fund depletion would be legally self-executing absent congressional action. The same lawyer should be careful before recommending a specific claiming age, retirement date, investment allocation, or household spending change unless that advice falls within the representation and the lawyer has the necessary competence or professional collaboration.

A useful AI-generated memo for the file would not say, "Congress will fix Social Security." It would say something closer to this: the client was advised using the June 2026 Trustees projection; the no-action scenario assumed a 22% OASI reduction beginning after Q4 2032; alternative legislative scenarios were discussed as uncertain; the client was told that scheduled benefits are not vested property rights under current Supreme Court doctrine; and no model output was presented as a guarantee of future law.

What This Means for Client Counseling Now

The calendar matters. Q4 2032 is close enough that a 60-year-old, a surviving spouse, a disabled worker's family, or an adult child helping with elder care may make decisions today that will still be playing out when the projected cut arrives. It is far enough away that Congress may act, and any single legislative forecast should be treated with caution. That combination is exactly why scenario planning is more useful than reassurance.

Lawyers do not need to become actuaries to use AI well in this area. They do need to know what the model is measuring. Is it estimating a dollar reduction from a stated percentage? Is it ranking legislative proposals by historical similarity? Is it summarizing policy options? Is it identifying clients whose reliance on benefits makes them vulnerable? Each of those tasks carries a different evidentiary weight.

The best counseling will sound less dramatic than the headlines. It will tell clients that the 2026 Trustees Report gives a current depletion projection, not a final political outcome. It will tell them that Social Security benefits are deeply relied upon, but not constitutionally vested in the way many people assume. It will use AI to make the planning file more complete, not to decorate uncertainty with false precision.

AI forecasting is valuable here because it can help lawyers prepare clients for several futures at once: no action, late action, partial reform, or a broader legislative package. Its professional value depends on keeping the legal premise visible. The strongest model in the office cannot change Flemming, cannot override the Antideficiency Act, and cannot make scheduled benefits payable if Congress leaves the trust fund short.

References

- Watchdog sounds Social Security alarm after 22% cut confirmed for 2032, Fortune, June 9, 2026.

- Social Security Reform: Legal Analysis of Social Security Benefit Entitlement Issues (RL32822), EveryCRSReport.

- Social Security Funding Crisis, Rutgers Law.

- No State Spared: Mapping the Impact of Social Security's Insolvency, Committee for a Responsible Federal Budget.

- Social Security benefits: What may happen if Congress doesn't act, CNBC, March 20, 2026.

- Using AI for Predictive Analytics in Litigation, American Bar Association, October 2024.

- Can AI Predict Case Outcomes? Legal Predictive Analytics Explained (2026), NexLaw, 2026.

Comments

Join the discussion with an anonymous comment.