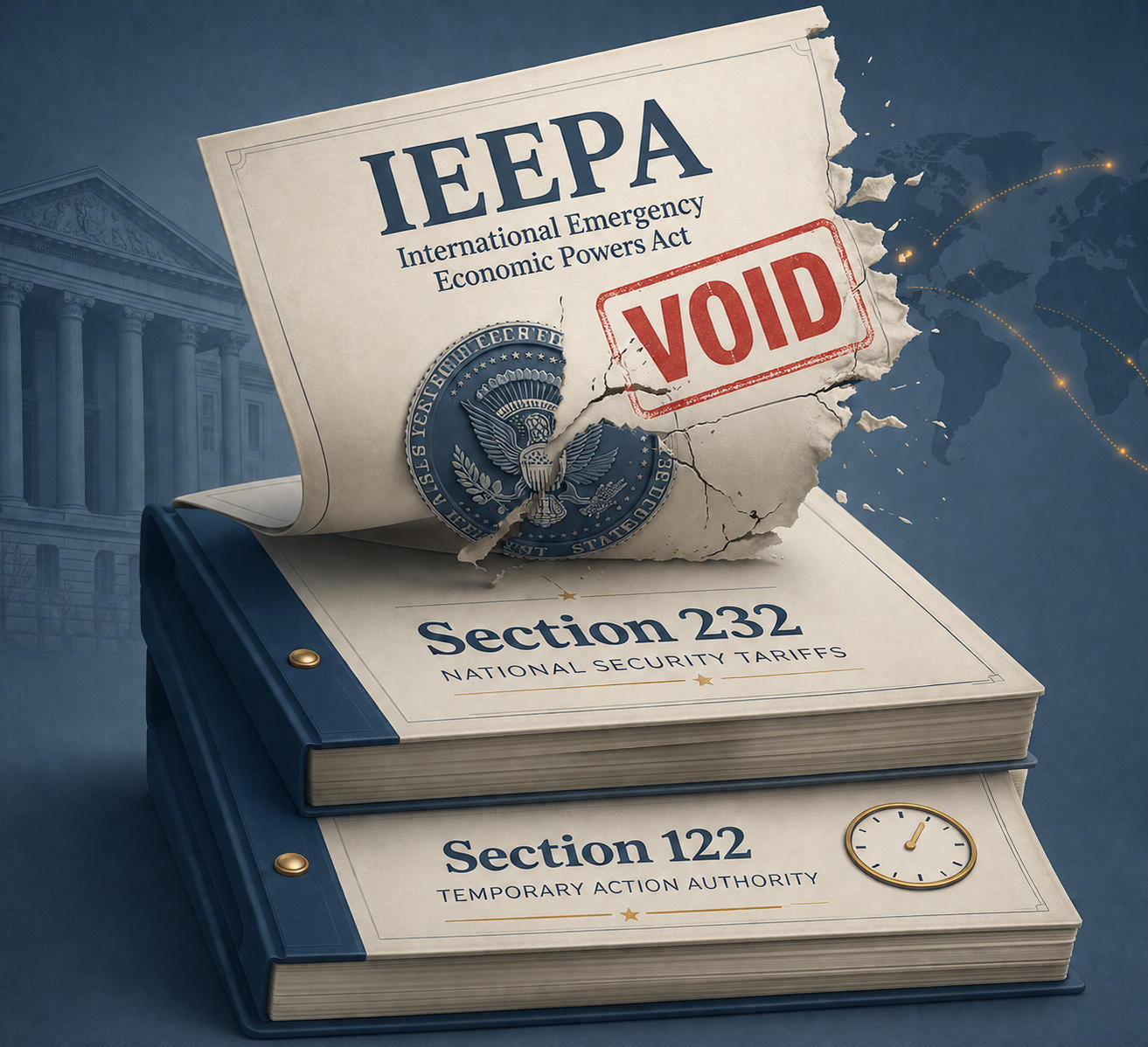

For a Canadian shipment entering the United States in Q3 2026, the first question is not whether the Supreme Court struck down President Trump’s Canada tariffs. It is which legal authority is attached to the duty line. The IEEPA-based layer is gone after Learning Resources, Inc. v. Trump, but that does not make the entry duty-free. Section 122 may still matter for non-exempt goods during its short statutory window, and Section 232 remains the larger practical exposure for steel, aluminum, autos, copper, lumber, trucks, buses, and any products brought into later national-security actions.[1][2][3]

For importers, the practical legal impact is this: one presidential theory failed, but several tariff lines can still survive liquidation because they rest on different statutes.

Current Tariff Status For Canadian Goods

| Tariff layer | Current Q3 2026 status | Canadian goods most affected | Practical compliance point |

|---|---|---|---|

| IEEPA tariffs | Revoked after Learning Resources; no continuing authority for IEEPA tariff collection | Previously covered Canadian goods subject to emergency-based tariff measures | Review past entries for possible refund paths, but do not assume automatic repayment before the CIT and CBP processes are clear |

| Section 122 temporary duty | Temporary 10% global duty imposed after the ruling; Section 122 is capped at 15% and limited to 150 days unless Congress extends it | Non-exempt goods, with CUSMA-compliant goods treated more favorably in the available Canadian-exporter analysis | Confirm whether the entry is within the effective window and whether a claimed exemption applies |

| Section 232 steel | Unaffected by Learning Resources; 50% rate reported for Canadian steel since June 2025 | Steel and steel derivative products within the covered scope | Classify carefully and separately from any IEEPA refund analysis |

| Section 232 aluminum | Unaffected by Learning Resources; 50% rate reported for Canadian aluminum since June 2025 | Aluminum and aluminum derivative products within the covered scope | Check product scope and derivative coverage before forecasting landed cost |

| Section 232 autos | Unaffected by Learning Resources; 25% rate reported | Autos and covered automotive products | Treat as a distinct national-security tariff line, not as a revived IEEPA measure |

| Section 232 copper | Unaffected by Learning Resources; 50% rate reported | Covered copper products | Monitor scope and any related investigation developments |

| Section 232 lumber | Unaffected by Learning Resources; 10-25% rate range reported | Covered lumber products | Do not assume CUSMA status removes separate Section 232 exposure |

| Section 232 trucks and buses | Unaffected by Learning Resources; reported as part of the surviving Section 232 program | Covered trucks, buses, and related products | Track product-specific effective notices and classification treatment |

The table is deliberately organized by authority rather than by headline. A purchasing team may ask whether Canadian inputs are now cheaper. The legally useful answer is narrower: IEEPA duties should no longer be collected after revocation, but entries that fall under Section 232 or the temporary Section 122 measure still need a duty calculation.

What Learning Resources Actually Removed

On February 20, 2026, the Supreme Court held 6-3 that IEEPA does not authorize the president to impose tariffs. The Court read the statute’s power to “regulate importation” as not encompassing taxation and treated tariff authority as a congressional power under Article I, Section 8.[1]

That matters because the invalidated duties were not struck down as unwise trade policy or as too burdensome for Canadian suppliers. They failed because the statute the administration used did not carry the tariff power the administration claimed. The same day, Executive Order 14389 revoked the IEEPA-based tariffs and the administration shifted to a temporary Section 122 duty.[2][4]

The separation-of-powers point is not academic for an importer. It explains why one duty line can be refund-sensitive while another remains collectible on the same shipment. A Canadian steel component could have been touched by an emergency tariff theory that is now invalid, while the steel-related Section 232 line remains on an entirely different statutory footing.

Stanford Law’s analysis framed the decision as restoring the historical understanding that tariff power belongs to Congress, and that is the broader constitutional significance. For entry work, the narrower consequence is enough: IEEPA is no longer a valid tariff hook, but the ruling does not cancel every tariff imposed during the same trade conflict.[5]

Why Section 122 Is A Different, Temporary Problem

Section 122 of the Trade Act of 1974 is not IEEPA with a different label. It is a trade statute that permits temporary import measures after presidential findings tied to a balance-of-payments emergency. The available post-ruling alerts describe the replacement duty as a 10% global duty, subject to a 15% ad valorem cap and a 150-day limit unless Congress extends it.[4]

That timing is already uncomfortable in Q3 2026. A duty that is legally temporary can still be live long enough to affect purchase orders, bonded entries, valuation reviews, and customer pricing. Norton Rose Fulbright’s Canadian-exporter analysis also notes that the practical impact is limited in part because the 10% duty is lower than the IEEPA rates and because CUSMA-compliant goods are exempted; the same research materials identify roughly 38% of Canadian exports as shielded from the Section 122 tariff by CUSMA compliance.[2]

That is an exemption question, not a mood. Importers still need origin support, product classification, and entry documentation consistent with the claimed treatment. If a sales team hears “IEEPA tariffs struck down” and assumes all Canadian-origin goods now move without added duty, the compliance team has to pull the conversation back to the tariff authority actually printed on the entry.

Section 232 Survived Because It Was Never An IEEPA Case

Section 232 duties rest on the Trade Expansion Act of 1962, not on the emergency-power theory rejected in Learning Resources. Osler states the practical point directly: the decision does not affect tariffs imposed under Section 232.[3]

That leaves substantial Canadian exposure in place. The research materials identify Section 232 rates of 50% on Canadian steel and aluminum since June 2025, 25% on autos, 50% on copper, 10-25% on lumber, and additional coverage for trucks and buses.[3]

| Question counsel should ask | Why it matters |

|---|---|

| Is the duty line based on IEEPA, Section 122, or Section 232? | The answer determines whether Learning Resources directly affects the charge |

| Has the entry liquidated? | Refund and protest options depend heavily on liquidation status and timing |

| Is the product within a Section 232 scope or derivative provision? | Section 232 exposure can survive even where IEEPA relief exists |

| Is CUSMA treatment claimed and supported? | CUSMA compliance may affect Section 122 exposure but does not itself erase Section 232 |

| Is there a pending investigation or product expansion? | Future Section 232 measures would not be invalid merely because IEEPA tariffs failed |

There are challenges to the expanded Section 232 program, and prior court treatment should not be turned into a guarantee. But as of Q3 2026, the importer’s working assumption should be that Learning Resources does not supply a direct defense to Section 232 collection. Any Section 232 challenge has to be evaluated on its own statute, record, and procedural posture.

Refunds: Possible Does Not Mean Automatic

The refund issue is where overconfident commentary can do real damage. The Court of International Trade has indicated statutory authority to order refunds of unlawfully collected IEEPA duties, and CBP is developing a Consolidated Administration and Processing of Entries system, or CAPE, to administer affected entries.[3][4][6]

That does not mean every importer should expect a clean, automatic deposit back to its account. The process is still being shaped by the CIT and CBP, and the available practitioner materials continue to emphasize preservation of rights, including protests within 180 days of liquidation.[3][4][6]

The immediate work is document work. Importers should identify entries that included IEEPA-based duties, separate those entries from Section 232 charges, check liquidation status, reconcile surety and broker records, and evaluate with counsel whether protest filings or other preservation steps are needed. For unliquidated entries, the question may be how CBP will process refunds or reliquidations. For liquidated entries, the calendar can become the controlling fact.

- Build an entry population by tariff authority, not just by country of origin.

- Flag entries with IEEPA duty deposits separately from entries carrying Section 232 duties.

- Track liquidation dates and the 180-day protest period for potentially affected entries.

- Preserve broker communications, payment records, classification support, origin documentation, and post-summary correction history.

- Avoid representing expected refunds as final recoveries until the procedural route is confirmed.

For companies with large Canadian programs, this is also a finance-control issue. Accruals tied to invalid IEEPA duties may need a different treatment from ongoing Section 232 exposure. The lawyer’s answer to finance should probably not be a single refund number until the entry set has been divided by authority and liquidation status.

CUSMA Helps, But It Is Not A Universal Shield

CUSMA compliance matters most in this post-ruling map because it can affect exposure to the temporary Section 122 duty. It does not answer every tariff question. A good may qualify under CUSMA rules and still require a separate Section 232 analysis if the product falls within steel, aluminum, auto, copper, lumber, truck, bus, or derivative coverage.

The July 1, 2026 CUSMA review adds political and legal uncertainty around the durability of North American trade preferences, but that uncertainty should not be confused with a current change in every duty line. CBC’s coverage of the review shows the agreement is under pressure; it does not itself replace the entry-by-entry statutory analysis.[7]

The Forward Risk Is Still Statutory

The next wave of exposure is unlikely to announce itself as “IEEPA 2.0” if the administration wants a more durable legal path. Osler identifies ongoing Section 232 investigations into copper, timber, semiconductors, pharmaceuticals, trucks, and aircraft, any of which could produce additional tariffs that would not fall merely because Learning Resources rejected IEEPA tariff authority.[3]

That does not mean every investigation will produce a tariff, or that every future Section 232 action will withstand challenge. It means the monitoring list should be organized by product and authority. A semiconductor input from Canada presents a different risk profile from a lumber shipment, and a temporary Section 122 duty presents a different litigation and timing profile from an existing Section 232 measure.

The disciplined Q3 2026 position is therefore limited but important: Learning Resources is a major constraint on presidential emergency tariff power and opens refund possibilities for IEEPA duties. It is not broad relief from Canadian tariff exposure. Section 232 duties remain the main surviving burden for many covered products, and Section 122 has been used as a short-term replacement mechanism while the refund process for past IEEPA collections continues to take shape.

References

- Learning Resources, Inc. v. Trump — Supreme Court of the United States, February 20, 2026

- US Supreme Court strikes down IEEPA tariffs, but practical impacts for Canadian exporters limited — Norton Rose Fulbright

- U.S. court overturns President Trump’s IEEPA tariffs: implications for Canada-U.S. trade — Osler

- United States terminates IEEPA-based tariffs following Supreme Court decision — White & Case

- President Trump’s Tariffs and the Separation of Powers at the Supreme Court — Stanford Law School

- IEEPA Tariffs on Canada, China, Mexico, Venezuelan Oil — Sandler, Travis & Rosenberg

- CUSMA review — CBC News

Comments

Join the discussion with an anonymous comment.