The 2026 AI chip selloff starts with dates, not mood. On June 1, the Bureau of Industry and Security clarified that US AI chip shipment bans applied not only to Chinese companies in China, but also to Chinese-headquartered companies operating through overseas subsidiaries.[1] Two trading days later, on June 3, the iShares Semiconductor ETF fell about 10%, and one market-data analysis put the single-session loss across AI chip stocks at roughly $1.4 trillion.[2]

That was the first wave. The second arrived from June 23 through June 26, when the market continued repricing semiconductor exposure and separate market reports described a broader AI-stock selloff spreading from Wall Street to Asia, with another estimate putting the multi-session loss at about $1.3 trillion.[3][4] By June 26, reporting on the megacap rebound noted that Nvidia and Alphabet were not participating in the bounce as chip stocks remained under pressure.[5]

The third wave, on July 6 and July 7, came after weeks of selling had already turned semiconductor exposure into a regulatory question. Reuters reported on July 6 that hedge funds had dumped chip stocks for a fourth consecutive week as AI shares sold off.[6] The legal overhang did not clear: on July 14, Commerce official Jeffrey Kessler said that “regulatory action on chips and AI is coming,” while also confirming that there was no replacement for the rescinded AI Diffusion Rule.[7]

Those facts do not prove legal causation in the way a court finding would. They do, however, make a tighter chronology than the generic “AI bubble” explanation permits. The selloffs followed identifiable export-control actions and official statements. The market mechanics were real, too: crowded positioning, DeepSeek-style competition fears, doubts about AI infrastructure spending, and broader technology rotation all mattered. But the sanctions-law timeline supplied the triggers that turned semiconductor enthusiasm into a compliance-horizon problem.

The Three Selloff Waves Were Dated Legal Events Before They Became Market Narratives

| Selloff wave | Regulatory or legal event | Market reaction reported | Narrow reading |

|---|---|---|---|

| June 3, 2026 | June 1 BIS clarification that AI chip shipment bans apply to Chinese firms’ overseas subsidiaries.[1] | SOXX fell about 10%; one analysis estimated roughly $1.4 trillion erased in the session.[2] | The market had to reprice a compliance perimeter that was wider than many investors appeared to assume. |

| June 23-26, 2026 | Market digestion of the subsidiary clarification, export-license limits, and broader chip-policy uncertainty. | Market reports described a cross-market AI stock selloff; another estimate put the wave at about $1.3 trillion.[3][4] | The second wave reflected not a new single rule, but the operational implications of the first trigger. |

| July 6-7, 2026 | Continued uncertainty around forthcoming chip and AI regulatory action. | Reuters reported hedge funds had dumped chip stocks for a fourth week through July 6.[6] | Positioning pressure amplified legal uncertainty rather than replacing it. |

For legal professionals, the important part is not the size of the red candle. It is the regulatory sequence that made the red candle rational. A company advising on semiconductor exposure after June 1 was no longer dealing only with valuation risk, customer-demand risk, or China revenue risk. It was dealing with the possibility that an overseas affiliate structure could fall within the same export-control prohibition that investors had mentally confined to shipments into China.

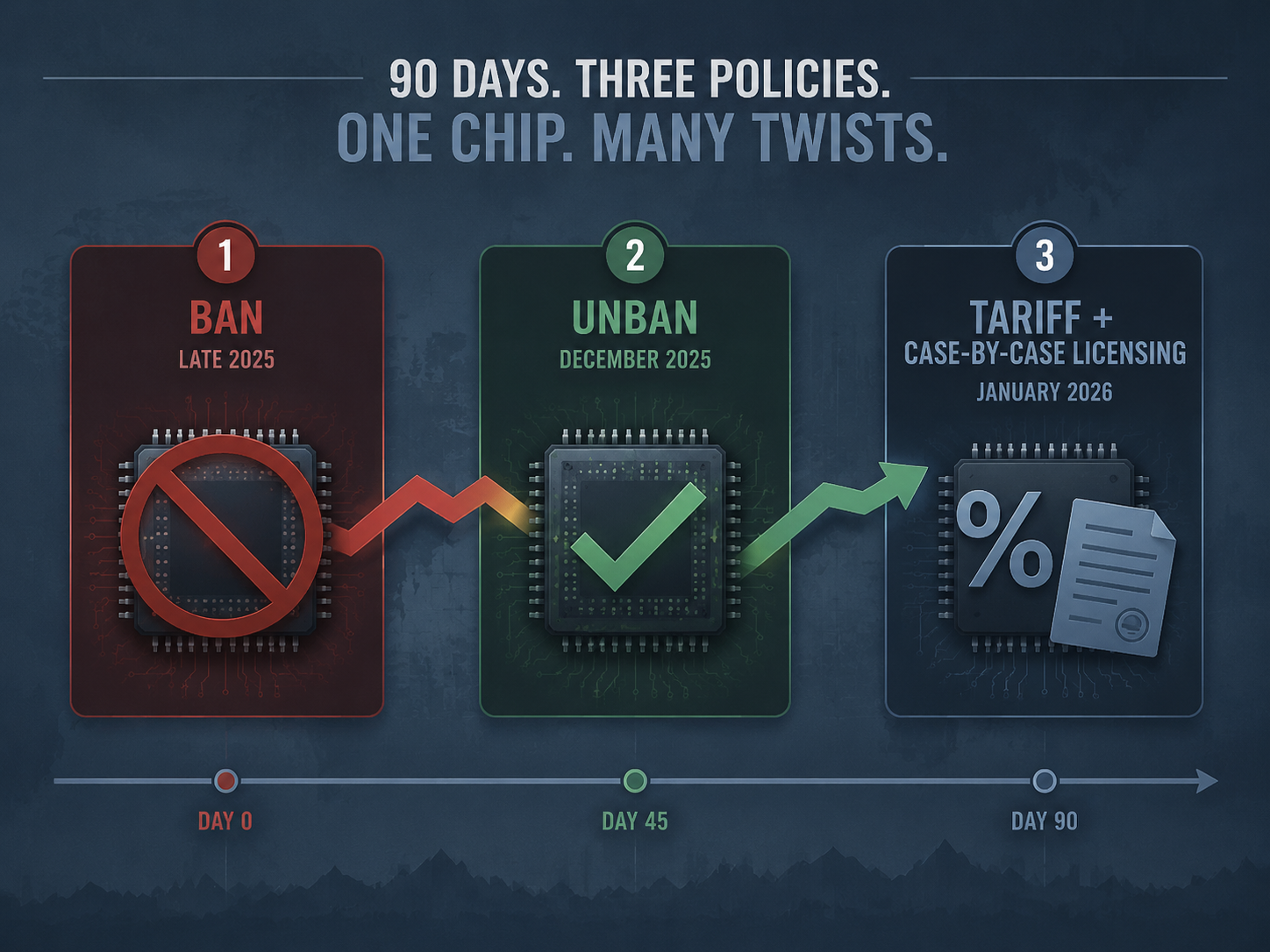

H200 Policy Had Already Trained the Market to Expect Reversal

The June selloff did not occur in a clean policy environment. By the time BIS clarified the subsidiary issue, the market had already watched the H200 chip move through three policy regimes in roughly 90 days: banned in late 2025, unbanned in December 2025, and then placed under a January 2026 framework involving a 25% tariff and case-by-case licensing.[8][9]

That sequence matters because “policy reversal” is too soft a phrase for what counsel had to translate. A ban is an exclusion point. An unban reopens a route but does not make it durable. A tariff changes economics without necessarily resolving the licensing question. Case-by-case licensing then moves the problem from a headline rule into an administrative queue, where individual facts, end users, destinations, and agency discretion matter.

The January 13 BIS final rule and January 14 Section 232 tariff action codified that H200 framework, according to legal and trade-law analyses.[8][9] For a trading desk, that might look like a policy compromise. For an in-house lawyer, it looks like a warning that revenue exposed to advanced AI chips can move from permitted to restricted to conditionally available inside one planning cycle.

That is the first underpriced risk. The market did not need a permanent prohibition to justify a lower multiple. It needed only a shorter compliance horizon and a credible reason to doubt that today’s permission would survive tomorrow’s rulemaking.

Annual Licenses Capped Certainty at 12 Months

The January 1, 2026 shift from Validated End-User exemptions to annual export licenses for TSMC, Samsung, and SK Hynix carried less market drama than the H200 reversal, but it changed the legal rhythm of semiconductor planning. The point was not that every license would disappear. The point was that the outer edge of certainty became 12 months.

That matters for contracts, disclosures, supply allocation, and board-level risk language. A VEU-style exemption can be understood, rightly or wrongly, as a more stable authorization architecture. An annual export license forces recurring review. Even if the renewal expectation is favorable, the company cannot advise customers, auditors, or investors as though the permission is indefinite.

The market often treats renewal risk as a footnote until the agency reminds everyone that the license is not a property right. In Q1 and Q2, that reminder sat underneath semiconductor valuations. In June, it became easier to price.

The June 1 Subsidiary Clarification Was the Sharpest Legal Trigger

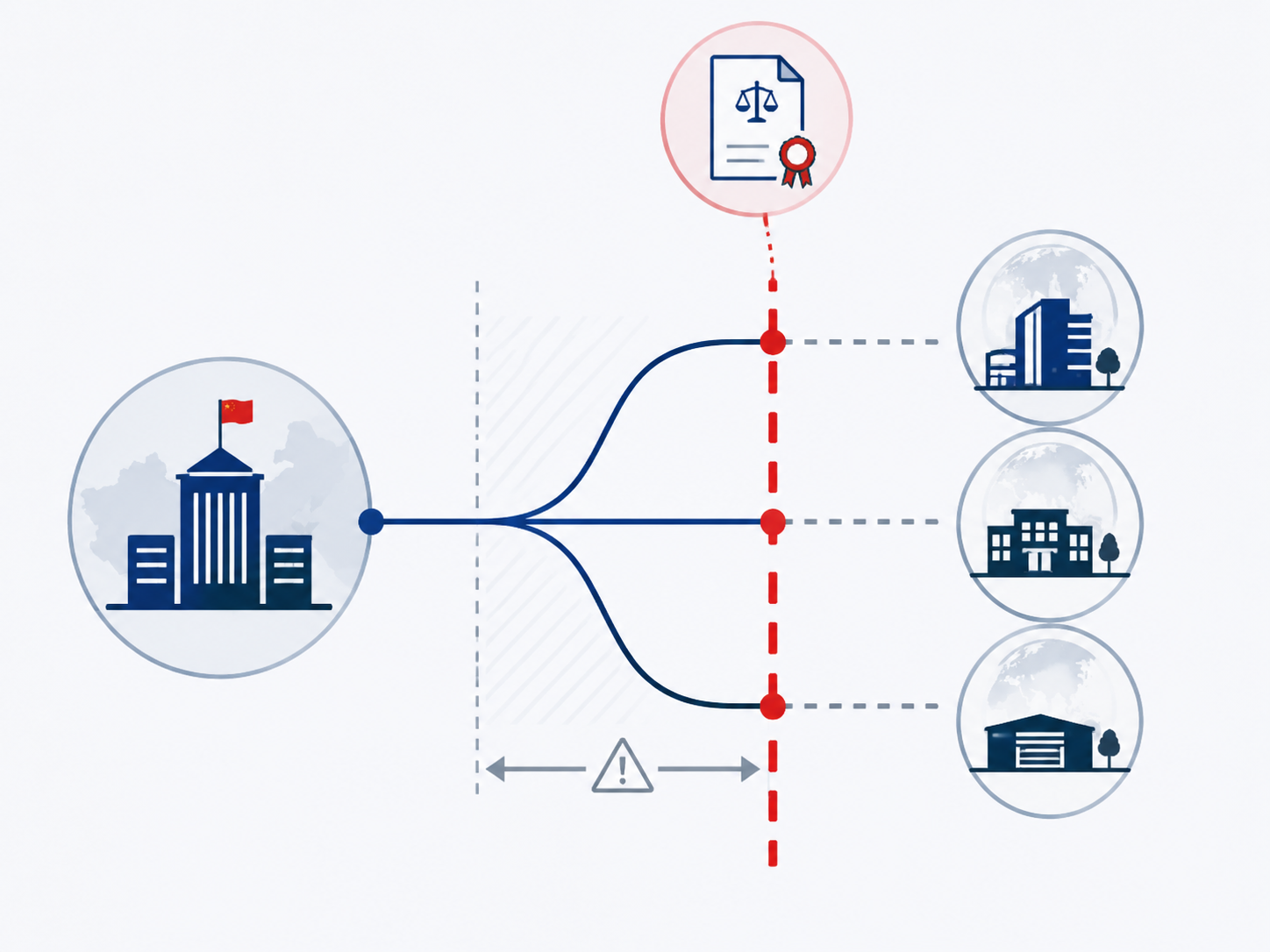

The June 1 BIS clarification deserves more attention than it received in broad market commentary. Al Jazeera reported that the United States said its ban on AI chip shipments applies to Chinese firms outside China, meaning Chinese-headquartered companies could not avoid the restriction merely by routing activity through overseas subsidiaries.[1]

That clarification did not need to create a new prohibition from nothing in order to move prices. Clarifications can be market events when they close a reading that counterparties had been using, or when they make enforcement risk visible to people who had treated it as remote. In this case, the legal object was narrow enough to describe cleanly: Chinese corporate control, overseas subsidiary activity, and AI chip shipment restrictions.

The June 3 market reaction followed quickly. Intellectia’s market analysis put the SOXX decline at about 10% that day and estimated roughly $1.4 trillion erased across AI chip stocks in the session.[2] That number should not be blended with later estimates from different windows. It is useful because it attaches a market response to a specific trading day immediately after a specific export-control clarification.

For counsel, the subsidiary point changes diligence questions. It pushes review beyond the shipping destination and into ownership, headquarters, affiliate relationships, end-use certifications, and the credibility of contractual representations. A supplier can no longer look only at whether the receiving entity sits outside mainland China. The corporate chain becomes part of the export-control analysis.

That is why the June 1 clarification is the cleanest bridge between legal text and the first selloff wave. It converted what may have looked like an edge-case compliance question into a market-wide semiconductor exposure question.

The Second Wave Was Compliance Digestion, Not Just Fresh Panic

The June 23-26 wave is harder to pin to a single new agency action, and it should not be forced into one. The better reading is that the market was digesting the consequences of the June 1 clarification together with the H200 instability and annual-license ceiling already in place.

The Guardian reported on June 23 that a US AI stock selloff was shaking markets from Wall Street to Asia.[3] FAQ.com.tw described the June 23-26 period as the worst semiconductor selloff of 2026 and estimated that AI chip stocks shed about $1.3 trillion during that wave.[4] CNBC then reported on June 26 that Nvidia and Alphabet sat out a megacap tech bounce as chip stocks sank.[5]

Those reports describe a broader repricing, not a one-document shock. By late June, the legal question had widened from “Does this shipment violate the rule?” to “How many revenue paths now require renewed diligence, agency approval, customer restructuring, or disclosure review?” That is slower work than a trading headline, and it tends to surface in stages.

This is also where non-legal market forces deserve their space. Hedge funds were crowded in AI-linked equities. DeepSeek-style competition anxiety had already made investors more willing to question the durability of US chipmakers’ margins. AI infrastructure spending was no longer being treated as costless inevitability. A regulatory trigger falling into that environment can produce a larger move than the same clarification would have produced in a calmer tape.

The distinction matters. The claim is not that sanctions law mechanically caused every dollar of the June 23-26 decline. The claim is that export-control developments supplied a traceable risk channel that the market had been too casual about, and the second wave reflected the delayed pricing of that channel.

By July, Positioning Pressure Met an Unresolved Rulebook

The July 6-7 selloff sits at the intersection of market positioning and regulatory ambiguity. Reuters reported on July 6 that hedge funds had dumped chip stocks for a fourth consecutive week as AI shares sold off.[6] That is not a sanctions-law fact by itself. It is evidence that the legal repricing had entered the portfolio-management layer, where risk reduction becomes self-reinforcing.

The rulebook still did not settle. On July 14, Reuters reported that Commerce official Jeffrey Kessler said “regulatory action on chips and AI is coming.” The same report said he confirmed there was no replacement for the rescinded AI Diffusion Rule.[7] The timing of that rescission is not entirely consistent across sources, with some accounts placing it in May 2025 and others in early 2026. The operational fact for Q3 2026 is narrower: as of Kessler’s testimony, the market had official confirmation that more action was coming without a replacement framework in place.

That is an uncomfortable posture for legal advisers. Pending legislation such as the GAIN AI Act, AI Overwatch Act, and STRIDE Act remained pending as of July 18, 2026, so they could not be treated as enacted law. At the same time, agency action was no longer hypothetical in the ordinary sense. Companies had to prepare for additional controls without pretending to know their final form.

What Legal Teams Had to Reprice

After June, the practical advice changed in several places at once. Semiconductor exposure could not be described only as a growth or concentration issue. It also implicated sanctions screening, export classification, customer diligence, licensing assumptions, subsidiary mapping, and disclosure controls.

- Customer and affiliate mapping: identify whether a non-China buyer is owned, headquartered, controlled, or functionally directed by a Chinese parent.

- License-horizon review: separate revenue supported by durable authorization from revenue dependent on annual renewal or case-by-case approval.

- Contract review: test whether sanctions, export-control, force-majeure, termination, and compliance-cooperation clauses actually cover a rapid policy reversal.

- Disclosure controls: evaluate whether China-linked AI chip exposure is described as a generic geopolitical risk when it has become a specific licensing and enforcement risk.

- Board reporting: distinguish market volatility from legal uncertainty that management can monitor, document, and escalate.

The last point is easy to underestimate. A board does not need counsel to predict the next stock move. It does need counsel to explain whether the company’s assumptions still match the current export-control perimeter. After the subsidiary clarification, a revenue model that treated offshore Chinese affiliates as ordinary foreign customers became harder to defend without additional diligence.

The Selloff Was Not a Pure Valuation Correction

There was froth in AI stocks. There was crowding. There were competition fears and spending doubts. None of that should be ignored. But the 2026 AI chip selloff is weaker as a pure market-correction story than as a sequence of regulatory repricings.

The H200 ban, unban, tariff, and case-by-case licensing sequence showed that advanced AI chip policy could reverse inside a short window. The move from VEU exemptions to annual export licenses shortened the certainty horizon. The June 1 subsidiary clarification widened the compliance perimeter. The June 23-26 wave reflected the market’s effort to absorb those consequences. By July, hedge-fund selling met official confirmation that more chip and AI regulatory action was still coming.

That is as far as the evidence supports going. It does not establish an adjudicated causal finding. It does support a disciplined chronological inference: sanctions-law actions repeatedly forced investors to reprice risks they had treated as secondary, and those repricings were load-bearing events in the 2026 AI chip stock selloff.

References

- US says ban on AI chip shipments applies to Chinese firms outside China, Al Jazeera, June 1, 2026.

- AI Chip Stocks Volatility June 2026: $1.4T Crash & Recovery Analysis, Intellectia.

- US AI stock sell-off shakes markets from Wall Street to Asia, The Guardian, June 23, 2026.

- AI Chip Stocks Shed $1.3 Trillion in Worst Semiconductor Selloff of 2026, FAQ.com.tw.

- Nvidia, Alphabet sit out megacap tech bounce as chip stocks sink, CNBC, June 26, 2026.

- Hedge funds dumped chip stocks for a fourth week as AI shares sold off, Reuters, July 6, 2026.

- Regulatory action on chips, AI is coming, Commerce official says, Reuters, July 14, 2026.

- Administration Policies on Advanced AI Chips Codified, Mayer Brown.

- Reported Draft Rules Signal New Semiconductor Export Controls Framework, Global Trade & Sanctions Law.

Comments

Join the discussion with an anonymous comment.