Last reviewed: July 18, 2026. CBP’s CAPE process for IEEPA duty refunds is still being phased in, and this analysis reflects the Phase 1 rules and public guidance available as of Q3 2026.

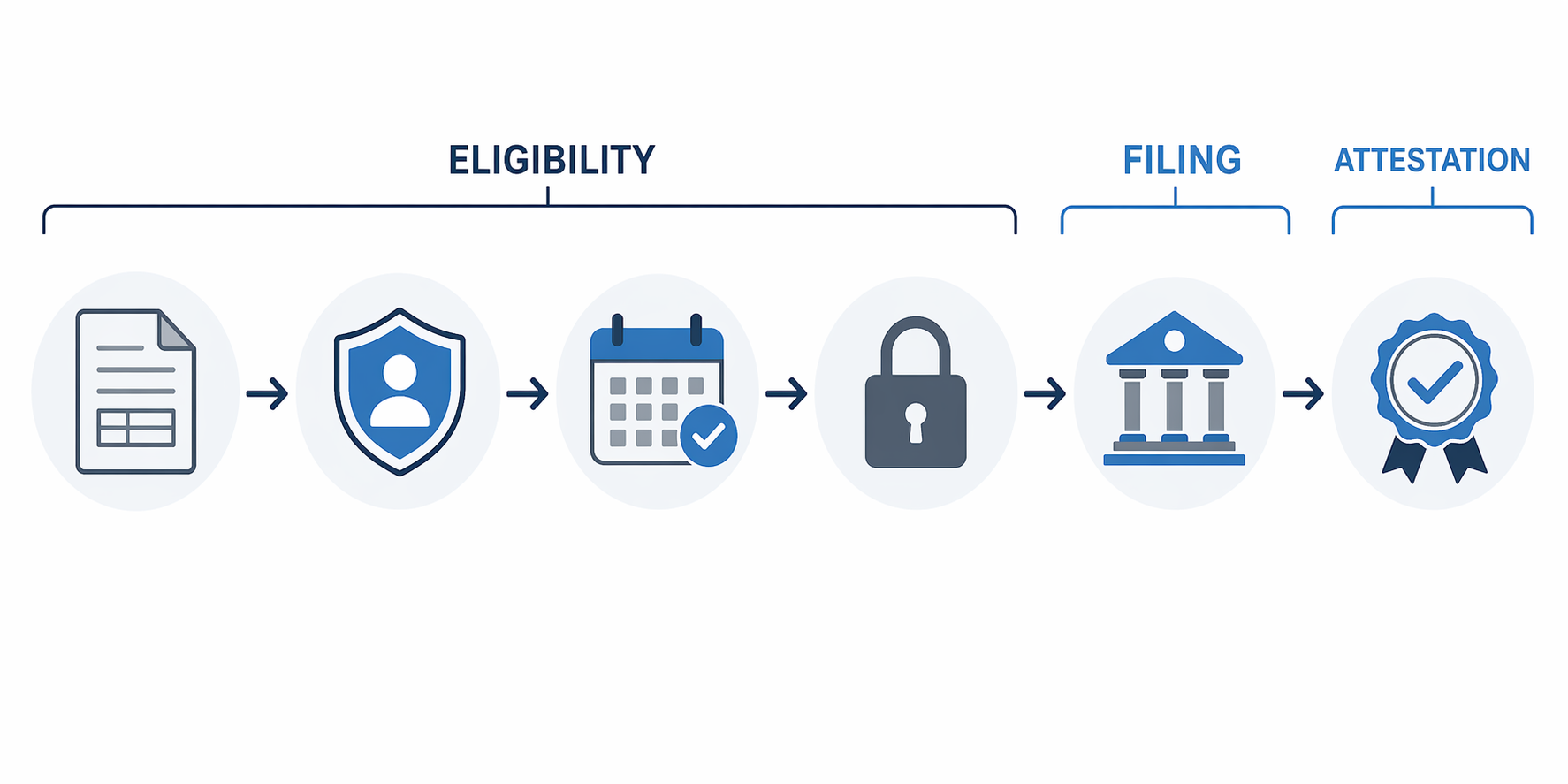

The first tariff refund eligibility requirement is not economic harm. It is legal capacity to file. Under CBP’s CAPE process, the claimant is the importer of record or an authorized customs broker acting for that importer; a customer that absorbed a tariff surcharge in a contract price does not become the filer merely because it ultimately bore the cost.[1][2]

That distinction is where many refund conversations should slow down. A procurement team may see a surcharge. A sales team may see a customer credit issue. A finance team may see a receivable from the government. But CBP is looking at entry records, liquidation status, importer authority, banking enrollment, and a certification that reaches classification, valuation, and country of origin. The refund request is not just a payment instruction; it is a customs filing.

What Phase 1 Actually Covers

CBP’s official IEEPA Duty Refunds guidance is the controlling starting point for the mechanics. Phase 1 covers unliquidated entries and entries within 80 days of liquidation. Entries with final liquidation, open protests, drawback claims, or antidumping and countervailing duty involvement are not part of the current Phase 1 path and are awaiting later phases that CBP had not announced as of July 2026.[1]

The timing matters because CAPE is not a universal reopening tool. An entry’s commercial importance, the amount of IEEPA duties paid, or the company’s view of fairness does not cure an entry-status problem. Before a company debates whether a refund is worth pursuing, someone has to confirm that the entry falls inside the current procedural gate.

| Question | Phase 1 Compliance Significance |

|---|---|

| Who may file? | The importer of record or its authorized customs broker, not downstream customers. |

| Which entries are currently in scope? | Unliquidated entries and entries within 80 days of liquidation. |

| Which entries are outside Phase 1 for now? | Entries with final liquidation, open protests, drawback claims, or AD/CVD involvement. |

| What must be ready before payment? | CAPE validation, ACH refund enrollment, filing authority, and support for the required attestation. |

| What is the central legal risk? | Unsupported statements about classification, valuation, origin, or eligibility can create enforcement exposure. |

The scale explains the pressure on trade teams. CBP collected about $166 billion in IEEPA duties across 53 million entries from roughly 330,000 importers. By early May 2026, 126,237 CAPE claims had been submitted, and 86,874 had passed initial validation. As of April 9, 2026, 56,497 importers had completed ACH refund enrollment, representing $127 billion in potential recoveries.[1]

Those figures do not prove that every enrolled importer has a clean claim. They show why executives, lenders, auditors, and customers may ask for quick action. They also show why the attestation should not be treated as a formality delegated to whoever has the login.

The Importer-of-Record Rule Is the Hard Edge

The importer-of-record limitation is not an administrative nuisance. It is the line between a customs refund process and a commercial reimbursement dispute. Benesch’s tariff refund Q&A emphasizes that the importer of record is the party positioned to claim refunds through the CBP process, while downstream customers who paid tariff-related charges generally have to look to contract terms, credit arrangements, or litigation theories rather than a direct CAPE filing right.[2]

That means the company whose cash flow is most affected may not be the company with filing authority. A U.S. importer may have passed a surcharge to a distributor; the distributor may have passed it to retailers; retailers may have passed some portion to consumers. CAPE does not trace those economics through the supply chain. It asks who was the importer of record on the entry and whether that filer can support the declaration.

For in-house counsel, this creates two separate workstreams. The first is the customs filing analysis: entry scope, status, authority, documentation, and attestation. The second is the commercial allocation analysis: contracts, customer communications, surcharge language, indemnity provisions, and refund-sharing clauses. Mixing the two is how a refund opportunity becomes an avoidable dispute.

The Filing Is Built Around Data Validation, Not Just a Claim Amount

CAPE validation begins with the entry data CBP already has, but the filer still has to make choices and declarations. Thomson Reuters describes CAPE as a process that requires global trade teams to coordinate systems, entry records, broker data, and payment readiness rather than simply submit a lump-sum refund request.[3]

A practical pre-filing review should start at entry level. The importer should identify the entries believed to include IEEPA duties, confirm whether they are unliquidated or within the 80-day post-liquidation window, remove entries outside Phase 1, and reconcile the importer-of-record number, broker authority, duty amounts, and entry summaries against internal records. If a broker will file, the authorization should be current and specific enough to support the action being taken.

ACH enrollment is also more than a banking afterthought. CBP’s reported enrollment figures show that refund payment readiness is already a major operational gate.[1] Companies that wait until after internal approval to discover banking or account-access gaps may find that the calendar, not legal theory, controls the filing sequence.

Records That Should Be Reconciled Before Submission

- Entry summaries and line-level IEEPA duty amounts.

- Liquidation status and dates, including whether the entry falls within the current Phase 1 window.

- HTSUS classification support, including prior rulings, product descriptions, engineering materials, or classification memoranda where relevant.

- Valuation support, including invoices, assists, royalties, related-party pricing materials, and adjustments reflected on the entry.

- Country-of-origin substantiation, including supplier declarations, production records, bills of materials, and origin analyses.

- Broker authorization, account access, and ACH refund enrollment readiness.

Baker Tilly’s refund readiness checklist points in the same direction: the work is not limited to locating duty payments, but extends to documentation that can withstand review if CBP asks why the importer was entitled to the refund and whether the underlying entry information was accurate.[4]

The Attestation Is Where Refund Eligibility Becomes Enforcement Risk

CBP’s CAPE process requires a declaration attesting to the accuracy of information including classification, valuation, and country of origin.[1] That language is the reason compliance officers should resist treating the filing as a treasury exercise. The agency is not only being asked to return money; it is receiving a certified statement about entry-level customs facts.

Diaz Trade Law’s analysis warns that refund filings can draw review to the underlying entry data, including classification discrepancies, valuation issues, and country-of-origin questions.[5] NYU Compliance & Enforcement similarly emphasizes that the end of a tariff collection theory does not erase enforcement risk tied to statements made during the refund process.[6]

The legal exposure is not abstract. False or unsupported certifications may implicate criminal statutes addressing false statements and customs fraud, including 18 U.S.C. §§ 1001, 542, and 545; civil penalties under 19 U.S.C. § 1592; and False Claims Act exposure under 31 U.S.C. § 3729(a), particularly where a claimant seeks payment from the government based on materially inaccurate information.[2][5][6]

The practical question is therefore not only whether IEEPA duties were paid. It is whether the importer can stand behind the entry information that supports the refund. If a product’s HTSUS classification has been debated internally for years, if origin support depends on outdated supplier statements, or if related-party valuation adjustments were not consistently reported, the refund filing may put those weaknesses in front of CBP under a certification.

A Pre-Filing Review Should Have a Named Owner

Someone inside the importer should own the reconciliation before the CAPE Declaration is filed. In some companies that will be trade compliance; in others it will be legal with broker support; in others it will require finance, tax, customs, and supply chain to work from a shared entry population. What matters is that the filer can explain who reviewed the data, what exceptions were found, how they were resolved, and why the remaining entries were included.

The review does not need to become a full customs audit of every import program before any claim is filed. It does need to be proportionate to the certification. A small entry set with consistent products, stable suppliers, and recent classification work presents a different risk profile from a large claim spanning multiple business units, brokers, product families, and origin scenarios.

Do Not Import Section 301 Rules Into CAPE

IEEPA CAPE refunds should not be conflated with Section 301 refund procedures. Section 301 refunds operate under separate mechanisms, including post-summary correction and protest timing rules, while CAPE is a CBP process developed for IEEPA duty refunds after the February 20, 2026 Supreme Court ruling and subsequent Court of International Trade orders.[1]

That distinction matters in internal communications. A company that tells business units it is “filing tariff refunds” without identifying the duty program, entry window, and governing procedure can create false expectations. The same product, supplier, or customer may be touched by more than one tariff regime, but the refund pathways are not interchangeable.

Open Protests, Drawback, AD/CVD, and Final Liquidation Remain Waiting Rooms

CBP has left significant entry categories for later phases. As of July 2026, Phase 2 scope, timing, and eligibility rules had not been announced for entries with open protests, drawback claims, AD/CVD involvement, or final liquidation.[1] Companies should avoid treating those entries as lost or recoverable until CBP provides the next set of instructions.

The safest internal label for those entries is “pending procedural guidance,” not “ineligible forever” and not “ready to file.” They should be inventoried separately, with the reason for exclusion from Phase 1 documented. That preserves the ability to act if CBP opens a later path without contaminating the current filing population.

Customer Claims Are Commercial Risk, Not CAPE Eligibility

Downstream disputes deserve attention, but they should not displace the customs analysis. J.S. Held describes a developing wave of refund-related disputes in which customers and business partners may argue over who should benefit from tariff recoveries.[7] Benesch likewise flags the possibility that customers may seek recovery where tariff costs were passed through.[2]

Holland & Knight has identified tariff-related consumer class action developments, including unjust enrichment theories, but those cases were still early-stage as of mid-2026 with few merits rulings.[8] That is an important caveat. The existence of filed claims does not establish that customers have a direct CAPE right, that refund recipients must automatically pass through recoveries, or that any particular theory will succeed.

The better compliance posture is to keep the issues separate while making sure they speak to each other. Customs teams should determine what can be filed and supported. Legal and commercial teams should review contract language, invoice disclosures, surcharge descriptions, customer commitments, and public statements before the company decides how to communicate any recovery.

A Practical Filing Sequence

The sequence below is not a substitute for legal advice, but it reflects the order in which the risk usually appears. Starting with dollar size is tempting; starting with filer authority and entry status is safer.

- Confirm the importer of record and determine whether the importer or authorized broker will file.

- Build the entry population and separate Phase 1 entries from entries awaiting later CBP guidance.

- Reconcile liquidation status, IEEPA duty amounts, broker records, importer records, and account access.

- Review classification, valuation, and country-of-origin support before anyone approves the attestation.

- Confirm ACH enrollment and payment details before submission.

- Document who reviewed the filing population, which exceptions were removed, and why the remaining entries were submitted.

The most useful file is not a presentation showing the maximum refund estimate. It is a workpaper that lets a reviewer trace each claimed entry from duty payment through eligibility, declaration support, and payment readiness. If CBP later asks why an entry was included, the importer should not have to reconstruct the answer from broker emails and spreadsheet versions.

What the CAPE Opportunity Really Requires

CAPE is a real administrative recovery path for IEEPA duties. It is also a controlled customs process that asks the importer of record to certify facts the agency can examine. The companies best positioned to use it are not necessarily those with the largest estimated refund, but those with clean entry-level records, clear filing authority, current banking enrollment, and enough classification, valuation, and origin support to make the attestation responsibly.

References

- IEEPA Duty Refunds, U.S. Customs and Border Protection.

- Tariff Refund Q&A: What to Do Now and What Legal Issues Lay Ahead, Benesch Law.

- The CAPE Tariff Refund System Is Here: Is Your Global Trade Team Ready?, Thomson Reuters.

- IEEPA Tariff Refund Readiness Checklist, Baker Tilly.

- Navigating IEEPA Tariff Refunds: Legal and Compliance Considerations, Diaz Trade Law.

- IEEPA Tariffs Are Dead. Enforcement Risk Is Not., NYU Compliance & Enforcement, March 20, 2026.

- IEEPA Tariff Refunds: Clarity on Eligibility, Complexity in Recovery, and a New Wave of Disputes, J.S. Held.

- Tariff Consumer Class Actions, Holland & Knight, June 2026.

Comments

Join the discussion with an anonymous comment.