A law firm that increased its technology budget by 39.3% from 2021 to 2025 is no longer making a small experimental bet. It is carrying a materially larger cost base into every pricing conversation, partner compensation discussion, client pitch, and renewal cycle.[1] That is the practical entry point for any serious discussion of the Nvidia vs AMD AI chip stock forecast for law firms: not which stock wins the quarter, but what the divergence between these companies says about the timing, scale, and negotiability of legal AI investment.

This is not investment advice, and it is not a recommendation to buy or sell Nvidia, AMD, or any other security. Chip-maker financials are useful here only as operational risk signals. They show where AI infrastructure capacity is concentrated, where pricing pressure may emerge, and how much uncertainty sits beneath the legal AI tools firms are being asked to adopt.

The budget question is sharper in 2026 because many firms are spending more before they have clean proof that generative AI has changed the economics of legal service delivery at scale. A pilot that makes a few lawyers faster is one thing. A firmwide platform commitment that touches research, drafting, knowledge management, matter intake, litigation support, and client-facing work product is something else. The first can be funded from an innovation line. The second must survive procurement, information security review, professional responsibility scrutiny, training costs, vendor lock-in concerns, and the managing partner’s question: why now?

Why Chip Stocks Belong In A Law Firm Budget Discussion

Most law firms will never buy an H100, MI300X, or MI400 GPU directly. They will buy legal AI software, research platforms, document tools, workflow systems, and cloud-hosted services. Those vendors will buy from cloud providers or infrastructure platforms. The cloud providers will absorb, finance, allocate, and price scarce GPU capacity. By the time the cost reaches a law firm invoice, it has passed through several layers of margin and contract design.

That indirect path does not make chip economics irrelevant. It makes them slower, less transparent, and more political. A vendor may not reduce prices when its GPU cost falls; it may use the savings to widen margin, add features, subsidize enterprise sales, or fund model experimentation. A cloud provider may discount GPU instances for strategic customers while holding list prices steady elsewhere. A legal AI vendor may be technically able to run inference on more than one chip stack, but contractually tied to one hyperscaler. These details determine whether infrastructure competition becomes a law firm saving, a vendor margin expansion, or no visible change at renewal.

For a 3-5 year planning calendar, the question is therefore not whether Nvidia or AMD has the more attractive stock chart. The question is whether Nvidia’s dominance gives firms enough platform stability to start building capability now, while AMD’s acceleration gives firms enough leverage to avoid overcommitting to today’s cost structure.

Nvidia’s Signal: Stability, Scarcity, And Near-Term Dependence

Nvidia’s current position is the cleanest argument against waiting for perfect clarity before adopting AI tools. It held an 81% AI chip share in 2026, according to Silicon Analysts, and its ecosystem remains deeply tied to CUDA, the software layer many AI developers have built around for years.[2] For law firms, that maturity matters because legal AI vendors usually choose infrastructure for reliability, developer availability, model compatibility, and enterprise support before they optimize for the lowest theoretical chip cost.

The revenue scale reinforces the point. Reuters reported Nvidia FY2026 data center revenue of $193.7 billion, representing 90% of total revenue and up 68% year over year. The company also guided Q2 FY2027 revenue to about $91 billion, above the $86.84 billion consensus cited in the same report, and announced an $80 billion share buyback.[3] Those are not legal-sector facts, but they are relevant procurement facts: vendors building enterprise AI products are not betting on a marginal supplier when they build on Nvidia-heavy infrastructure.

The less comfortable part is scarcity. Reuters also reported that Nvidia’s supply obligations rose to $119 billion in Q1 FY2027 and quoted CEO Jensen Huang saying the company was supply-constrained “through the entire life of Vera Rubin.”[3] If a legal AI vendor depends on Nvidia-backed capacity, capacity scarcity can show up as higher prices, tighter usage limits, slower enterprise rollouts, or premium pricing for high-volume clients. The firm may never see a line item labeled “GPU scarcity,” but it can still pay for it.

That makes Nvidia’s dominance a two-sided planning signal. It lowers implementation ambiguity for early adoption because the ecosystem is mature, widely supported, and familiar to AI engineering teams. It also gives vendors and cloud providers a credible reason to treat high infrastructure pricing as the baseline rather than a temporary inconvenience.

AMD’s Signal: A Credible Second Source, Not A Settled Cost Reset

AMD’s importance for law firm planning is not that it has become an equal substitute in every workload. The important signal is that the market is beginning to treat AMD as a credible second source for AI infrastructure. AMD’s 114% year-to-date stock surge in 2026 is the headline, but the operational data behind that enthusiasm is more useful than the surge itself.

AMD’s data center revenue reached $5.8 billion in Q1 2026, up 57% year over year, and its data center GPU revenue was projected to reach $15 billion in 2026 from roughly $7-8 billion in 2025.[4] Tech Insider projected the MI400 series alone at $7.2 billion in first-year revenue.[5] Those numbers are still far smaller than Nvidia’s data center scale, but they change the procurement conversation from “there is only one serious infrastructure path” to “how quickly can second-source competition affect terms?”

The validation signal matters because large AI buyers are not casual reference customers. Silicon Analysts reported that Meta runs 100% of Llama 405B inference on MI300X, Microsoft runs GPT-3.5/4 inference on MI300X, and OpenAI committed to a 6GW MI450 deal.[2] Those examples do not prove that every legal AI workload will move cleanly to AMD. They do suggest that AMD’s role is no longer confined to slideware or speculative roadmaps.

Pricing is the reason legal operations teams should pay attention. Silicon Analysts placed MI300X pricing at $10,000-$15,000 compared with H100 pricing at $25,000-$40,000, and cloud GPU pricing at $1.50-$6.98 per hour for MI300X compared with $1.99-$12.29 per hour for H100. The same source frames this as a 15-40% cost advantage.[2] For a law firm, that range should be treated as a conditional planning range, not a promised saving. It can only reach the firm if cloud providers expose the economics, vendors multi-source effectively, model performance remains acceptable, and contracts allow the benefit to move downstream.

Where The Cost Actually Passes Through

A law firm invoice for AI rarely maps neatly to the cost of a GPU hour. The firm may pay per seat, per matter, per document, per query, per workflow, per data room, or under an enterprise license with usage bands. That packaging is convenient for adoption but inconvenient for cost diagnosis. If infrastructure costs fall, the savings may be hidden unless the firm has negotiated usage transparency, benchmarking rights, price review triggers, or renewal leverage.

| Layer | What Changes At That Layer | What The Law Firm Should Watch |

|---|---|---|

| Chip supplier | GPU availability, chip pricing, software ecosystem maturity | Whether Nvidia scarcity persists and whether AMD becomes a dependable second source |

| Cloud provider | Instance pricing, committed-use discounts, capacity allocation, custom silicon strategy | Whether AMD-backed capacity appears in enterprise terms, not just public benchmarks |

| Legal AI vendor | Model hosting choices, inference cost, margin, product packaging, service levels | Whether the vendor can multi-source without degrading performance or security posture |

| Law firm | Seat pricing, usage caps, workflow economics, renewal pressure | Whether contracts convert infrastructure competition into lower unit costs or better terms |

The most useful procurement question is not “Do you use Nvidia or AMD?” A vendor can answer that question truthfully and still reveal very little. Better questions are: which workloads run on which infrastructure, whether the vendor can shift inference workloads without retraining the product, whether usage pricing changes when lower-cost GPU capacity is used, and whether the customer receives any benefit from cloud cost reductions during the contract term.

This is also where CUDA dependency and ROCm maturity become more than engineering vocabulary. CUDA’s maturity reduces vendor execution risk. ROCm’s progress may create pricing leverage, but migration work, performance tuning, developer familiarity, and support depth still matter. A legal AI vendor that was built and optimized around Nvidia infrastructure may not be able to capture AMD economics quickly, even if AMD list pricing is attractive. Spheron’s 2026 comparison of ROCm and CUDA treats the ecosystem gap as a central issue rather than a footnote.[6]

What The Stock Forecasts Actually Add

Analyst targets are useful here mostly because they display uncertainty. Zacks tracked 47 analysts with an average Nvidia target of $304.77 and a range from $180 to $500; it tracked 37 analysts with an average AMD target of about $492 and a range from $320 to $755.[7] Those ranges are too wide to support a tidy operating forecast for a law firm. They are, however, a reminder that the market itself is still debating the durability of Nvidia’s pricing power and the speed of AMD’s share gains.

Valuation data points in the same direction. The research brief identifies Nvidia at about 23x forward earnings with a PEG ratio of 0.68, while AMD trades around 70x forward earnings. Those figures do not tell a law firm what AI tool to buy. They do suggest that investors are pricing Nvidia as a dominant platform with large near-term earnings and AMD as a faster-growth challenger whose future share gains must still be proven.

For legal technology planning, that distinction is valuable. Nvidia’s forecast profile supports confidence that the dominant infrastructure ecosystem will remain available for pilots, knowledge tools, and early production use. AMD’s forecast profile supports caution before signing broad, long-duration contracts that assume today’s GPU economics are permanent. Neither forecast supports freezing AI investment until the market settles.

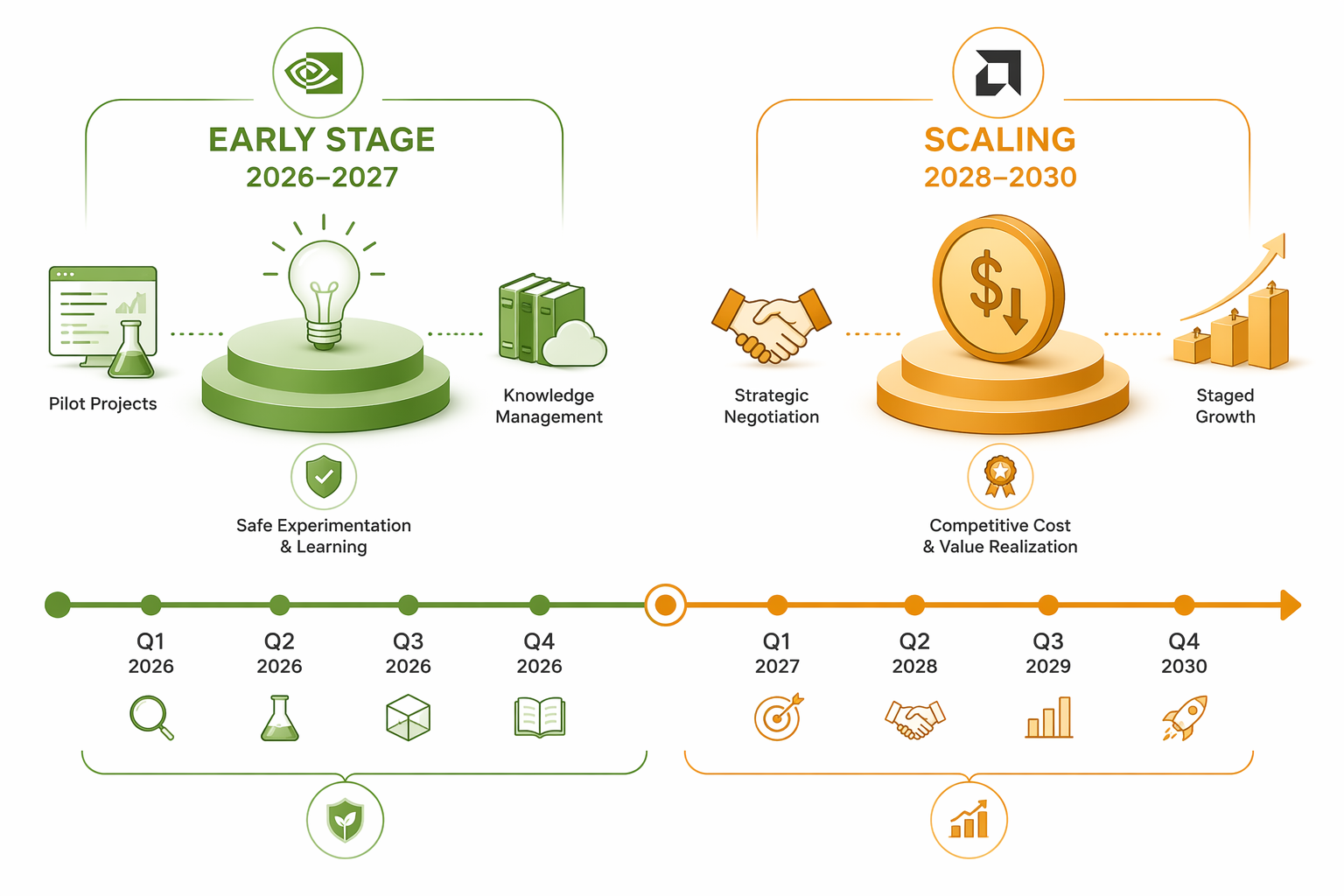

A 2026-2030 Timing Framework For Law Firms

The sensible 2026 posture is not maximal acceleration and not passive waiting. Firms need enough adoption to learn which workflows benefit, which lawyers change behavior, which data controls are required, and which vendors can survive enterprise scrutiny. That work is easier to justify on mature Nvidia-backed platforms because the near-term risk is less about chip abandonment and more about whether the firm can turn AI access into measurable workflow change.

| Planning Window | Primary Signal | Appropriate Firm Posture |

|---|---|---|

| 2026-2027 | Nvidia platform maturity and continuing supply constraints | Run serious pilots and limited production deployments in research, knowledge management, drafting support, and workflow testing |

| 2027-2028 | AMD second-source credibility and cloud pricing visibility | Negotiate shorter renewal cycles, usage transparency, and price-review mechanisms |

| 2028-2030 | Actual pass-through of AMD competition, custom silicon, and vendor multi-sourcing | Scale firmwide only where unit economics, adoption behavior, and risk controls are proven |

Early-stage use should favor learning velocity over perfect cost optimization. Research assistance, internal knowledge retrieval, first-draft generation, clause comparison, diligence triage, and litigation workflow testing can expose the operational blockers that matter long before the firm debates full deployment. The firm learns which practice groups have repeatable use cases, where human review remains the bottleneck, and whether vendor outputs can be integrated into existing document, billing, and matter-management systems.

The broader commitment decision should be held to a higher standard. A firmwide license with aggressive minimums, long renewal tails, or fixed usage economics can trap the firm in a cost structure just as second-source pressure begins to matter. If AMD-backed capacity produces meaningful cloud discounts, and if vendors can actually run legal AI workloads across multiple infrastructure stacks, the negotiating environment in 2028 may look different from the one in 2026. The difference is not guaranteed, but it is material enough to avoid unnecessary rigidity.

What To Ask Before A Multi-Year AI Contract

- Which cloud provider and GPU infrastructure support each major workload, including inference-heavy features?

- Can the vendor move workloads across Nvidia, AMD, or other infrastructure without changing security, performance, or service commitments?

- Does the contract include usage reporting detailed enough to distinguish adoption failure from infrastructure-driven cost growth?

- Are price reviews, benchmarking rights, or most-favored pricing protections triggered if cloud GPU pricing declines?

- What happens if the vendor’s preferred model provider, cloud provider, or GPU stack changes during the contract term?

These are not exotic questions. They are the AI version of questions firms already ask about hosting, data residency, uptime, conflicts systems, and document-management integrations. The difference is that AI infrastructure costs can move quickly, while law firm contracts often move slowly.

The 15-40% Cost Advantage Should Change Negotiations, Not Budgets Overnight

The 15-40% AMD cost advantage reported by Silicon Analysts is meaningful, but it should not be inserted into a law firm ROI model as a guaranteed future discount.[2] At most, it belongs in scenario planning. One scenario assumes Nvidia-backed pricing remains sticky because the legal vendor market values maturity, support, and compatibility. Another assumes AMD competition reaches cloud contracts and legal AI vendors pass part of the benefit to customers. A third assumes savings are offset by migration costs, performance tuning, or vendor margin retention.

A disciplined budget model can hold all three possibilities without pretending to predict the chip market. For example, a firm considering a broad AI rollout can separate near-term capability-building spend from scale-dependent consumption spend. It can approve pilots and targeted deployments now while making the largest volume commitments contingent on usage data, negotiated unit economics, and vendor evidence that infrastructure competition is visible in pricing.

That distinction matters because ROI failure in legal AI will not come only from high infrastructure cost. It can also come from low lawyer adoption, poor workflow fit, weak matter-level measurement, overbroad licensing, insufficient training, or risk controls that make the tool too cumbersome to use. Lower GPU pricing helps only after the firm has proven that the work should be done through the tool in the first place.

The Macro Context Is Big Enough To Create Distortion

The semiconductor and AI infrastructure market is large enough that law firms should expect turbulence rather than a smooth cost curve. Intellectia cited Bank of America’s estimate of the semiconductor industry at $1.3 trillion in 2026 and noted that U.S. technology giants are spending more than $700 billion on AI infrastructure.[8] When hyperscalers are committing at that scale, legal-sector demand is not setting the market price. Law firms are downstream buyers in a market being shaped by cloud platforms, model labs, consumer AI products, advertising businesses, and enterprise software companies.

Custom silicon is the late-stage caveat that prevents overconfidence in either merchant GPU story. Google TPUs, AWS Trainium, Microsoft Maia, and other hyperscaler chips may limit the pricing power of both Nvidia and AMD over time. That does not mean merchant GPUs become unimportant. It means the 2027+ cost structure may depend on a three-way negotiation among Nvidia, AMD, and hyperscaler-owned alternatives rather than a simple two-company contest.

For law firm planning, the caveat is straightforward: do not build a five-year AI budget that assumes one supplier’s dominance, one challenger’s discount, or one cloud provider’s current economics will remain intact. The infrastructure layer is too strategically important, and the buyers above the legal sector are too large.

A Defensible Planning Posture

The operational reading of Nvidia vs AMD is clear enough for 2026 decisions even though the market forecast is uncertain. Nvidia’s dominance supports near-term experimentation and selective production adoption because platform maturity lowers implementation risk. AMD’s acceleration supports negotiating caution because credible second-source competition may eventually change cloud GPU rates and legal AI vendor economics. Neither signal justifies waiting on the sidelines until infrastructure prices fall.

A law firm can act without pretending to be a semiconductor analyst. Build enough AI capability now to understand real workflows, adoption patterns, risk controls, and matter economics. Avoid contracts that lock the firm into one cost structure before AMD competition, cloud pricing, and ecosystem fragmentation become clearer. Revisit vendor economics at renewal with specific questions about infrastructure sourcing, usage reporting, and price pass-through.

References

- 2026 Report on the State of the US Legal Market: Analysis of AI bubble, Thomson Reuters / Georgetown Law, 2026

- AMD vs Nvidia AI GPU Market Share 2026, Silicon Analysts, February 2026

- Nvidia forecasts quarterly revenue above estimates, announces $80 billion share buyback, Reuters, May 20 2026

- Better Artificial Intelligence (AI) Stock Buy in June: Advanced Micro Devices vs. Nvidia, Motley Fool, June 11 2026

- AMD MI400 Series AI GPU Data Center 2026, Tech Insider, April 13 2026

- ROCm vs CUDA GPU Cloud 2026, Spheron, 2026

- NVDA Price Target Stock Forecast, Zacks, July 2026

- AI Chip Stocks Investment July 2026, Intellectia.ai, July 2026

Comments

Join the discussion with an anonymous comment.