The legal significance of the SEC’s March 17, 2026 crypto asset release is not that Bitcoin became easier to promote. It is that Bitcoin became easier to classify. For Bitcoin ETF regulation and legal compliance, the work has always turned less on enthusiasm for the asset than on whether counsel could identify the asset, the product wrapper, the exchange listing standard, the custody model, and the regulator with enough confidence to sign off on the next step.

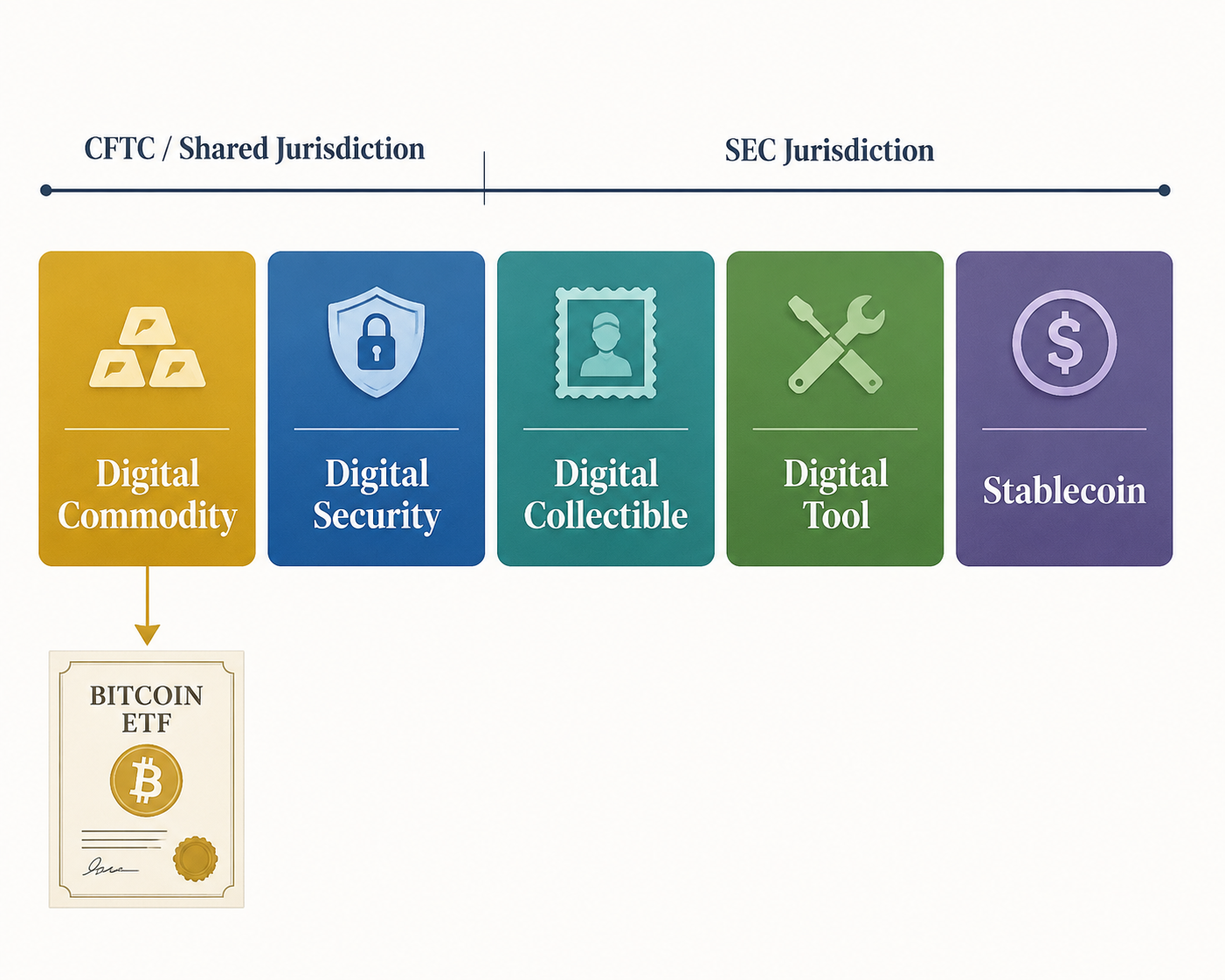

The SEC’s five-category taxonomy gives that analysis a better starting point. The release identifies digital commodities, digital collectibles, digital tools, stablecoins, and digital securities as distinct categories for applying federal securities laws to crypto assets.[1] That does not make every classification easy. It does, however, change the sequence of the inquiry. A lawyer no longer has to begin with the enforcement docket and work backward from complaints, settlements, and careful agency silences. The release supplies a classification framework first, then asks whether facts around issuance, sale, operation, or continuing managerial efforts bring the asset or transaction within securities law.

The Taxonomy Starts With Legal Function, Not Market Popularity

The release matters because it separates the crypto asset from the securities-law transaction that may surround it. That distinction is familiar in principle and maddening in practice. Under Howey, an investment contract analysis turns on the economic reality of a transaction: investment of money, in a common enterprise, with an expectation of profits derived from the efforts of others. The difficult question for crypto counsel has been whether an asset that was once sold through an investment contract remains stamped as a security forever.

The SEC’s March 2026 release addresses that “evergreen securities” problem directly. It explains how a non-security crypto asset may become subject to an investment-contract analysis and how that status may cease when the relevant facts no longer support the Howey elements.[1] That is the legal hinge for Bitcoin ETFs. The useful question is not whether a digital token can appear in a securities transaction. It can. The useful question is whether the asset in the ETF is itself treated as a digital security, or whether the ETF is a securities product holding a non-security digital commodity.

| SEC category | Legal effect for ETF and trading analysis | Practical consequence |

|---|---|---|

| Digital commodities | The asset is not treated as a digital security merely because it trades on crypto markets; Bitcoin falls here under the 2026 taxonomy.[1] | ETF counsel can analyze the fund as a securities product holding a commodity-like crypto asset, rather than as a fund holding a portfolio security. |

| Digital securities | The asset or transaction remains within federal securities law when the facts satisfy the securities-law framework, including investment-contract analysis.[1] | Listing, broker-dealer, custody, disclosure, and exchange questions become materially heavier. |

| Digital collectibles | The category recognizes assets whose primary function is distinct from capital-raising securities transactions.[1] | Classification still depends on how the asset is marketed, sold, and supported. |

| Digital tools | The category recognizes functional-use crypto assets separately from digital securities.[1] | Utility language is not dispositive; counsel still tests facts against Howey. |

| Stablecoins | The release treats stablecoins as a separate classification rather than forcing all payment or reserve-linked tokens into one securities bucket.[1] | Additional rulemakings, including mid-2026 stablecoin implementation work, may affect the category’s operating boundaries. |

The table should not be read as a safe-harbor chart. The release is an interpretive staff statement, not a statute, not a court decision, and not a final rule carrying the full force and effect of law. The SEC can still take a different position through rulemaking, enforcement, or later guidance. Courts can also reject or narrow the agency’s approach when a contested token classification is litigated.

Why Bitcoin’s Digital Commodity Classification Changes the ETF Analysis

Bitcoin’s placement in the digital commodity category is the cleanest part of the release for ETF purposes. The ETF itself is a security. Shares of a registered exchange-traded product still trade through the securities markets, with exchange rules, disclosure obligations, surveillance expectations, intermediaries, and investor-protection requirements. But the underlying asset is not being treated as a digital security under the taxonomy.[1]

That distinction resolves a practical problem that used to sit inside every Bitcoin ETF file. If the underlying Bitcoin were treated as a security, the product would raise a different set of questions: whether the fund was holding securities, whether custody arrangements satisfied securities-custody requirements for that asset type, whether intermediaries touching the asset needed different registrations, and whether exchange listing rules built for commodity-based trusts were the right fit. By classifying Bitcoin as a digital commodity, the SEC narrows those issues. The securities-law focus returns to the ETF shares and the market structure around them, rather than treating the underlying Bitcoin as a securities-law instrument.

This is not a declaration that Bitcoin is outside all regulation. It is a jurisdictional allocation. The SEC remains responsible for the securities product, the exchange listing, the broker-dealer activity, and the investor-facing disclosure regime. Commodity and derivatives oversight questions remain relevant where Bitcoin spot, futures, swaps, clearing, or market-integrity issues implicate the CFTC’s side of the ledger. The practical benefit is not the disappearance of regulators. It is a less artificial fight over which legal vocabulary applies at the threshold.

The Generic Listing Standards Needed a Classification Framework

The 2025 generic listing standards made the procedural path for crypto ETFs faster, but procedure was never enough by itself. Bitnomial described the September 17, 2025 rule changes as compressing the approval path from roughly 240 days to about 75 days by removing the need for a separate 19b-4 process for each qualifying product.[2] That kind of timing change matters to issuers and exchanges, but it does not answer the prior legal question: qualifying based on what classification of asset?

The March 2026 taxonomy supplies the missing substantive frame. A generic listing standard can reduce bespoke review only if the exchange, issuer, and SEC staff have a shared view of which assets are eligible for the pathway. Bitcoin’s classification as a digital commodity gives the listing analysis a defined asset category rather than an implied conclusion pulled from prior approvals.

That changes the legal work product. Exchange counsel can map the proposed listing to the generic standard and the digital commodity category. Issuer counsel can separate disclosure about the ETF’s securities from disclosure about Bitcoin’s commodity-like market risks. Compliance teams can design controls around creation, redemption, custody, valuation, and trading without simultaneously relitigating whether the underlying asset is a security every time the product file moves from one desk to another.

The speed of the process should not be mistaken for automatic approval. Generic standards still require a product to fit objective conditions. The taxonomy makes those conditions more administrable for Bitcoin because the asset classification is no longer inferred from enforcement history or market practice alone.

In-Kind Creation Was the Mechanical Precursor

The SEC had already moved Bitcoin ETP operations closer to commodity ETP mechanics before the taxonomy arrived. On July 29, 2025, the agency permitted in-kind creations and redemptions for crypto ETPs.[3] That matters because authorized participants and liquidity providers do not experience ETF regulation as an abstract classification exercise. They experience it through baskets, settlement, custody movements, cash substitutions, spread management, and operational exceptions.

In-kind creation and redemption allow the ETF ecosystem to handle the underlying asset more directly, rather than forcing every creation and redemption event through cash. For Bitcoin ETPs, that was a significant operational shift. It also made the later taxonomy more coherent: if the market structure is being administered in a way that resembles commodity ETP plumbing, the underlying legal classification should say plainly whether Bitcoin is being treated as a commodity-like digital asset or as a security.

There is still legal work inside the plumbing. Authorized participants must understand what they can touch, when they can touch it, which affiliate or custodian handles it, and how books and records reflect the movement. Broker-dealers need policies that distinguish ETF share activity from any direct crypto asset activity. Custodians need controls that satisfy the product’s disclosure and regulatory commitments. The taxonomy does not perform those tasks, but it gives them a more stable classification premise.

What the Howey Clarification Does for Non-Security Crypto Assets

The most important legal move in the release is not the naming of five boxes. It is the explanation of movement into and out of investment-contract treatment. Crypto classification has long suffered from a category error: a token sale might be a securities transaction, and then the token itself was discussed as though it had permanently absorbed that legal character. The SEC’s March 2026 interpretation tries to separate the asset from the scheme of distribution, ongoing managerial dependence, and purchaser expectations that may surround it.[1]

For Bitcoin, that separation is straightforward compared with many issuer-linked tokens. Bitcoin does not need an issuer’s continuing managerial program to explain its ETF eligibility under the taxonomy. For other assets, the analysis remains more demanding. A token labeled a tool, collectible, stablecoin, or commodity may still be sold or packaged in a way that creates an investment contract. Conversely, an asset that was distributed in a securities transaction may later be evaluated under different facts if the relevant Howey dependencies have fallen away.

That is a narrower, more useful conclusion than “crypto assets are not securities.” The release does not support that broad claim. It supports a transaction-sensitive analysis that allows non-security crypto assets to exist while preserving the SEC’s authority over securities offerings, securities intermediaries, investment products, and trading venues within its jurisdiction.

The SEC-CFTC MOU Helps, but It Does Not Eliminate Boundary Disputes

The March 11, 2026 SEC-CFTC memorandum of understanding is important supporting architecture. Latham & Watkins’ policy tracker describes the MOU as establishing six core areas of coordination between the agencies as they work toward a more unified approach to digital asset oversight.[4] That matters because Bitcoin ETF regulation sits precisely where agency boundaries become operational: securities product on one side, commodity-like underlying asset and related derivatives markets on the other.

Still, an MOU is not a jurisdictional amendment. It can improve coordination, reduce duplicative surprises, and give regulated entities a better sense of which agency is expected to lead on which issue. It does not prevent later disagreement over a particular token, exchange function, custody arrangement, or derivatives-linked product. Nor does it bind courts asked to decide whether an agency has exceeded statutory authority.

For Bitcoin ETFs, the MOU’s value is practical. It reinforces the idea that the SEC can regulate ETF shares and securities-market intermediaries without needing to characterize Bitcoin itself as a security. It also acknowledges that digital commodity markets require oversight coordination rather than a single-agency fiction.

Day-to-Day Compliance Consequences

The taxonomy’s immediate value is administrative. It gives each participant in the Bitcoin ETF chain a classification premise that can be written into procedures, reviewed by counsel, tested by auditors, and updated if the SEC changes course.

- ETF issuers can draft risk factors and eligibility analysis around a securities product holding a digital commodity, rather than treating the underlying Bitcoin as an unresolved securities-law question.

- Exchanges can connect Bitcoin ETF listing files to the 2025 generic listing pathway, while reserving bespoke analysis for assets that do not clearly fit the digital commodity category.

- Broker-dealers can separate activity in ETF shares from policies governing direct crypto asset handling, custody, or affiliate activity.

- Authorized participants can evaluate creation and redemption obligations against a clearer asset classification, especially after the 2025 in-kind approval.

- Custodians can align controls, disclosures, and contractual undertakings with Bitcoin’s treatment as a digital commodity held for a securities product.

The harder compliance work shifts to documentation discipline. A firm relying on the taxonomy should be able to show who classified the asset, what source they relied on, how the conclusion maps to the product structure, and what event would trigger reconsideration. For Bitcoin, that reconsideration trigger may be relatively remote. For other crypto assets, it may be central to the file.

Market Growth Is Context, Not Legal Authority

The market backdrop explains why this classification question became urgent, but it does not prove the legal point. Bitnomial reported that U.S. crypto ETFs had $42 billion in net inflows in 2025 and cited a pipeline of more than 126 ETF filings.[2] Those figures are useful as market context. They are not SEC findings, and they should not be treated as evidence that a product is legally eligible.

The distinction matters. A crowded filing pipeline can pressure the agency to regularize process, but it cannot supply statutory authority. Heavy inflows can demonstrate demand, but demand is not classification. The legal effect comes from the March 2026 release, the 2025 listing framework, and the operational permissions that allow the ETF structure to function.

The Strategic Plan Confirms Priority, Not Finality

The SEC’s FY 2026–2030 Draft Strategic Plan, released June 2, 2026, reinforces that digital assets are now a priority lane for the agency. Latham & Watkins’ tracker describes digital assets as the first regulatory objective under Goal 1, including priorities around clarifying securities-law boundaries and ensuring custody and trading services operate under appropriate oversight.[4]

That is meaningful, but it is not the same as a final rulebook. A strategic plan tells regulated entities where staff attention and agency resources are likely to go. It does not settle whether a specific token is a security, whether a particular custody structure is sufficient, or whether later rulemaking will preserve the taxonomy exactly as issued in March 2026.

Where the Framework Still Leaves Risk

The release reduces one kind of uncertainty and leaves several others intact. It reduces the old uncertainty created when classification had to be inferred from enforcement posture. It leaves intact the uncertainty that comes from staff-level interpretation, contested statutory boundaries, and the inevitable litigation of assets that do not look like Bitcoin.

- The taxonomy has not yet been tested in court.

- The SEC may revise the framework through formal rulemaking or take a different position in enforcement.

- SEC-CFTC coordination can reduce friction without eliminating statutory overlap.

- Stablecoin rulemakings underway in mid-2026 may add criteria that affect how that category operates.

- ICO-era and issuer-linked tokens may still require fact-specific Howey analysis even if the taxonomy provides better labels.

For Bitcoin ETFs, those residual risks are manageable because Bitcoin sits in the least issuer-dependent part of the taxonomy. For products built around other assets, the release is better understood as a disciplined starting point than as a clearance certificate.

The Current Operating Framework

The SEC has done something more useful than declare a winner in the crypto classification debate. It has given issuers, exchanges, broker-dealers, custodians, and authorized participants a framework that can be administered. Bitcoin is classified as a digital commodity. Bitcoin ETF shares remain securities. The generic listing standards provide the procedural route. In-kind creation and redemption provide a more conventional operating mechanism. The Howey clarification explains why not every crypto asset must remain trapped in a securities classification forever, while preserving the SEC’s authority where the facts support investment-contract treatment.

That is a major break from classification by lawsuit, press release, and implication. It is not the end of legal judgment. The March 2026 release is the current operating framework for Bitcoin ETF regulation and related legal compliance, subject to later rulemaking, litigation, and inter-agency friction. For now, that is enough to make Bitcoin ETF regulation easier to explain and easier to administer, without pretending the next boundary dispute has been legislated out of existence.

References

- SEC Clarifies the Application of Federal Securities Laws to Crypto Assets, SEC, March 17, 2026

- The ETF Approval Fast Lane, Bitnomial, March 2, 2026

- SEC Permits In-Kind Creations and Redemptions for Crypto ETPs, SEC, July 29, 2025

- US Crypto Policy Tracker, Latham & Watkins

Comments

Join the discussion with an anonymous comment.