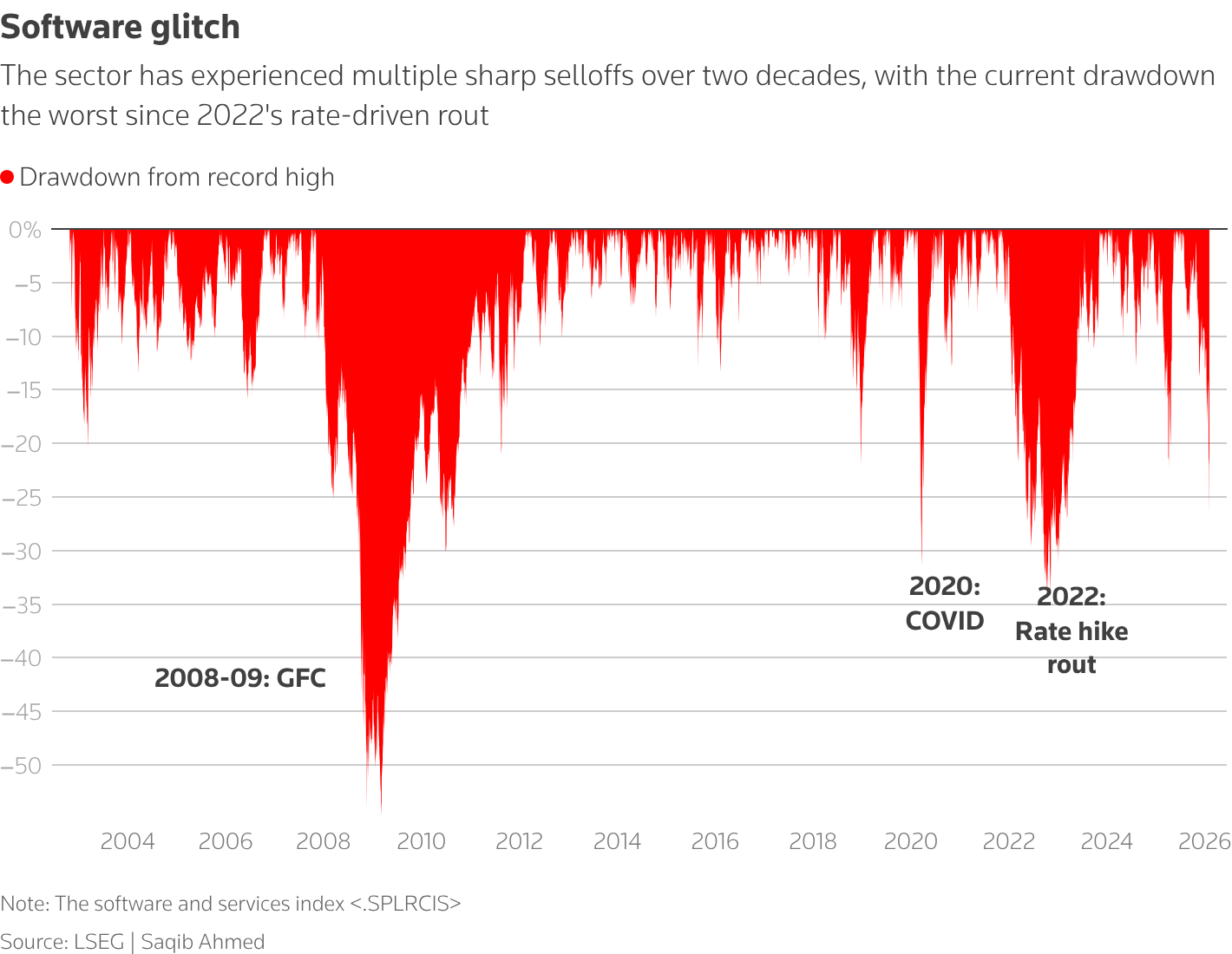

The February selloff was easy to read as another AI panic until the names on the screen made it harder to dismiss. Over six trading days, global software stocks lost about $830 billion in market value. Thomson Reuters fell 18% in a single day, its largest one-day drop on record; RELX dropped 14%, its biggest fall since 1988; Wolters Kluwer fell 13%; LegalZoom lost 19.7%; and FactSet declined 10.5%.[1]

Those were not law firm stocks. They were legal information, workflow, and data businesses. That distinction matters. A vendor sells subscriptions, tools, and data access; a law firm sells judgment, execution, risk transfer, and, still in many matters, time. But the market was reacting to something law firm leaders should recognize: a possible weakening of information scarcity as a pricing foundation.

The immediate trigger was Anthropic’s Claude Cowork legal plugin, described around capabilities that sit close to the work law firms and legal departments actually price and staff: contract review, NDA triage, and compliance workflow automation.[2] Those are not the glamorous corners of practice, but they are exactly where leverage, realization, and workflow control show up in the numbers. If investors suddenly questioned whether legal information companies could protect premium economics around those tasks, law firm CFOs should at least ask what the same repricing logic would reveal inside their own P&Ls.

The law firm exposure is not the stock price

No managing partner should take an 18% fall in Thomson Reuters shares and pencil in an 18% revenue risk for the firm. That is not how the exposure works. The parallel is structural, not direct.

The more useful question is this: if a market can punish legal information companies because AI might compress the value of research, review, and workflow bottlenecks, what happens to law firm economics when clients start applying the same skepticism to time, staffing, and rate increases?

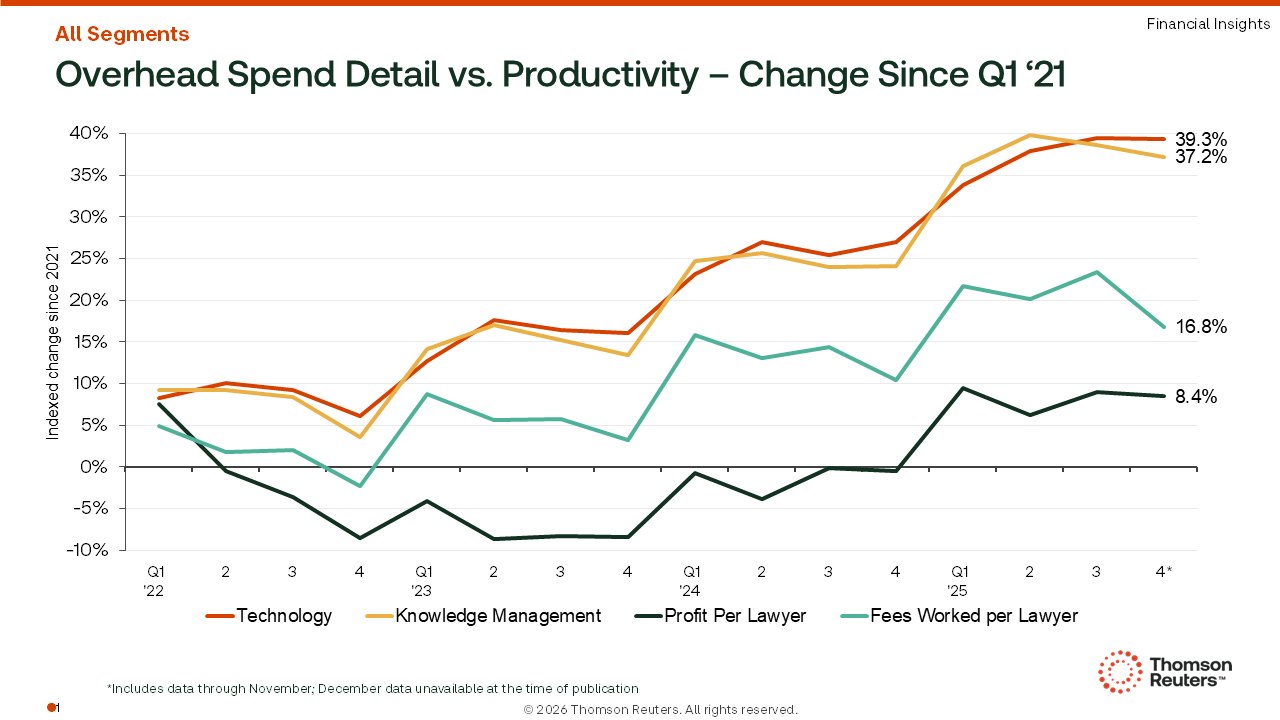

That question lands in an awkward year for law firm finance. The Thomson Reuters Institute and Georgetown 2026 State of the US Legal Market report says law firm technology spending has increased 39.3% since 2021, including a 9.7% jump in 2025 alone, described as the fastest recorded annual rise.[3] That is the kind of line item that begins as a strategic investment and, unless someone ties it to displaced hours, reduced cycle time, better realization, or lower cost of service, quietly becomes the new base cost.

The report’s warning is not that firms are currently weak. It is almost the opposite. The concern is that firms may be spending as if current revenue conditions are permanent rather than a temporary spike, and it models a correction scenario in which higher costs, weaker utilization, and rate pressure collide.[3] That is a finance problem before it is a technology problem.

A strong year can still hide a fragile engine

The hardest conversations in law firm finance rarely happen when the numbers are bad. They happen when the numbers are good for reasons nobody wants to interrogate.

On the surface, the legal market has had plenty to like. Profit per lawyer rose 8.4% above pre-2022 levels, according to the Thomson Reuters/Georgetown report.[3] But fees worked per lawyer climbed 16.8%, and the report ties the profit improvement more to rate growth than operational improvement.[3] In a partner meeting, that difference matters. A higher profit figure supported by pricing power is not the same as a higher profit figure supported by a lower cost to produce the work.

The rate story is no longer subtle. Am Law 100 rates crossed $1,000 per hour for the first time, and some partners charge $2,000 per hour, according to Thomson Reuters commentary on the pressure created when AI efficiency meets billable time.[4] At those levels, every claim about AI-enabled efficiency invites a client-side follow-up: if the tool shortens review, triage, drafting, or research, why does the bill still look built around the old production model?

First-quarter 2026 data from Wells Fargo added another layer. U.S. law firm revenues rose 13.1%, while rates rose 11.4%, expenses rose 9.7%, and headcount growth slowed to 3.3%.[5] Those are not recession numbers. They are numbers that show how much of the current lift still comes from pricing.

| Finance signal | What it measures | Why it matters for AI strategy |

|---|---|---|

| Technology spend up 39.3% since 2021 | Growth in law firm technology spending | AI and related systems are raising the expense base before many firms can prove displaced work |

| Technology spend up 9.7% in 2025 | Fastest recorded annual increase | The cost curve is steepening during a period still supported by strong rates |

| Profit per lawyer up 8.4% above pre-2022 levels | Profitability measure per lawyer | The headline looks healthy, but does not by itself prove better production economics |

| Fees worked per lawyer up 16.8% | Fees generated per lawyer | The improvement is tied heavily to pricing and workload, not necessarily efficiency |

| Q1 2026 rates up 11.4% | Billing rate growth | Current revenue momentum remains exposed if clients resist further increases |

This is the uncomfortable link between AI jitters in the stock market and law firm financial strategy. The selloff did not prove that legal AI will destroy incumbent economics. It did show how quickly capital can reprice a business when investors believe the old scarcity premium is less durable than assumed. Inside a law firm, the comparable repricing does not arrive as a ticker drop. It arrives through budget guidelines, panel reviews, write-downs, RFP questions, alternative fee demands, and partner compensation disputes over who gets credit when technology reduces the labor needed.

The billable-hour paradox is now a finance constraint

Law firms often describe AI as a productivity story while still managing associates, matters, and partner expectations through hours. That can work for a while, especially when demand and rates are strong. It becomes harder when the technology budget rises, clients ask for savings, and internal targets move in the opposite direction.

BigHand’s 2026 Law Firm Finance Report, a vendor-sponsored source and therefore one to handle with some caution, captures the contradiction clearly enough to be useful: 89% of firms reported increased write-offs, 64% reported declining billable hours, and 99% planned to increase billable-hour targets.[6] Those findings do not prove that AI caused the pressure. They do show the management pattern that makes AI savings difficult to convert into firm economics.

If a contract review tool reduces the hours needed for a first pass, the financial consequence depends on the model around it. Under a fixed fee, the firm may keep margin if quality holds and staffing is disciplined. Under an hourly model, the same improvement may reduce billable inventory unless the firm replaces the hours with higher-value work, changes the pricing arrangement, or absorbs the tool as a client expectation without recovering the cost.

This is where many AI programs become vague. They track licenses, pilots, training attendance, and use cases. They do not always track whether the tool changed leverage, realization, write-offs, staffing ratios, matter duration, or partner discounting behavior. A firm can be operationally busier, technologically more advanced, and financially less clear about which costs are supposed to come out of the system.

Clients are not yet seeing the savings they were promised

The client-side check is important because law firms do not get to declare efficiency unilaterally. ACC/Everlaw survey evidence says 59% of companies have seen no savings from outside counsel AI use. Because that is self-reported survey evidence, it should not be stretched into a universal verdict on law firm AI performance. It does, however, identify the question general counsel are already entitled to ask: where did the saved time go?

Some of the answer may be legitimate. Firms may be using AI to improve completeness, accelerate turnaround, reduce internal friction, or handle work that would otherwise sit in a bottleneck. Not every gain appears as a lower invoice. A faster compliance review or cleaner NDA process may matter to a client even if the immediate bill does not fall.

But that explanation has a shelf life. When technology is marketed as efficiency, clients eventually look for evidence in budgets, staffing plans, cycle times, or fee structures. If the firm’s answer is only that rates rose because the market allowed it, AI becomes part of the client’s rate challenge rather than the firm’s defense.

Work may move before revenue breaks

The more likely near-term pressure is not a dramatic collapse in demand for elite firms. It is a quieter movement of work to firms that can satisfy enough of the quality requirement at a lower blended rate.

The Thomson Reuters/Georgetown report’s mobile-demand pattern deserves attention here: midsize firms achieved 5% demand growth, compared with 2% for the largest firms, as clients shifted work downstream from $1,000-plus-per-hour firms.[3] That is not a wholesale rejection of premium counsel. Clients still pay for bet-the-company risk, specialist judgment, and board-level confidence. But it suggests that some work is already becoming more mobile when rate levels are difficult to justify.

AI can accelerate that movement if it narrows the execution gap on repeatable tasks. A midsize firm with disciplined workflows, credible AI-assisted review, and lower rates may not need to match an elite firm’s entire platform. It only needs to be good enough for the category of work the client is prepared to move.

For the largest firms, the risk is not that all work becomes commoditized. The risk is mix erosion. If lower-complexity review, triage, diligence, and compliance work moves away, the remaining book may still command premium rates but support a different leverage model. That affects associate development, utilization, matter profitability, and the internal economics of partners who built practices around large teams.

What a real AI finance review should test

A law firm does not need to respond to February’s selloff by freezing AI investment. That would be the wrong lesson. The better lesson is to stop letting AI sit only in the technology budget and start treating it as a test of the firm’s economic model.

The finance review should begin at the matter level, not the conference stage. For each meaningful AI use case, the firm should know what changes if the tool works: fewer associate hours, faster partner review, lower write-offs, shorter lockup, improved realization, better margins on fixed fees, or more capacity without proportional hiring. If none of those changes can be named, the initiative may still have strategic value, but it should not be booked mentally as a profit strategy.

- For contract review, test whether first-pass hours fall, whether partner review time changes, and whether write-downs move.

- For NDA triage, test whether intake-to-turnaround time improves and whether the work can shift to a lower-cost staffing model.

- For compliance workflows, test whether recurring tasks can be priced with more confidence under fixed or subscription-style arrangements.

- For research and knowledge tools, test whether lawyers reduce duplicative work or simply produce more internal drafts before billing the same way.

- For firmwide licenses, test adoption separately from financial impact; usage does not equal margin improvement.

The pricing director belongs in that review as much as the CIO. So does the practice leader who knows which partners will protect hours even when workflow changes. AI savings do not become firm economics by themselves. Someone has to decide whether the benefit goes to the client, the partner, the associate pyramid, the firm margin, or some negotiated mix of all four.

The modeled correction is a warning, not a forecast

There is a disciplined way to use the February selloff, and it is not to turn it into prophecy. Credible market voices, including Jensen Huang and JPMorgan’s Mark Murphy, argued that investors may have overreacted. They may be right. A six-day rout can contain real information and still overshoot.

The same restraint applies to the Thomson Reuters/Georgetown correction scenario. It is modeled, not predicted.[3] It does not say that law firm revenues are about to fall because vendor stocks fell. It says that if firms add cost on the assumption that today’s strong revenue environment will continue, they become more exposed to a change in rates, demand, utilization, or client tolerance.

That is enough. Law firm strategy in Q3 2026 does not need an apocalyptic AI thesis. It needs a finance discipline that asks whether technology spend is reducing the cost of producing legal work, improving the price the client will accept, or merely adding another permanent expense line to a model still dependent on rate growth.

The market repriced legal information businesses when the durability of their economics looked less certain. Law firms will not be repriced on an exchange in the same way. They will be repriced matter by matter, client by client, and budget cycle by budget cycle. The firms that understand that will treat AI less as a marketing claim and more as a stress test of whether spending can become efficiency before clients, utilization, and rates force the issue.

References

- Global software stocks hit by Anthropic wake-up call on AI disruption, Reuters, February 4, 2026.

- AI concerns pummel European software stocks, Reuters, February 3, 2026.

- 2026 Report on the State of the US Legal Market: Is there an AI bubble?, Thomson Reuters Institute.

- The $2,000/hour problem: When AI efficiency collides with billable time, Thomson Reuters.

- US law firm revenues surged again in first quarter, Wells Fargo says, Reuters, April 29, 2026.

- Legal AI productivity profitability paradox, BigHand.

Comments

Join the discussion with an anonymous comment.