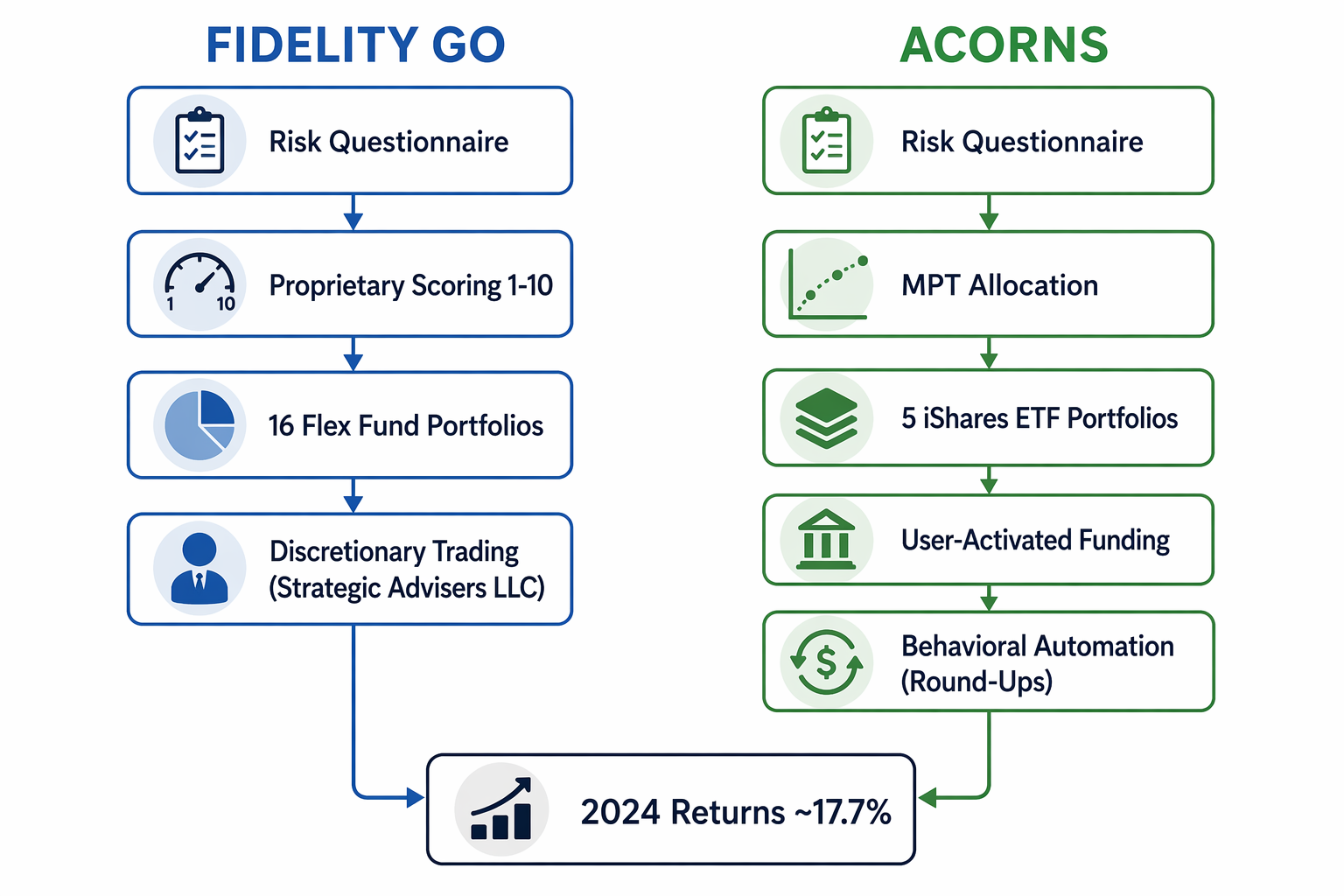

The most misleading fact in a Fidelity vs Acorns robo advisor comparison is also the most tempting one: in Condor Capital Wealth Management data reported by Investopedia, Fidelity Go’s 2024 equity return was 17.78%, while Acorns came in at 17.73%.[1] That five-basis-point spread is too thin to carry a serious judgment about which platform is “better,” and the period is only a single trailing-12-month window. It is useful anyway, because it clears the table. If performance did not meaningfully separate them in 2024, the harder question becomes what kind of automated decision-making the investor actually entered.

Neither platform needs to be treated as a consumer-facing “AI product” for the comparison to matter. The relevant automation is mostly embedded in portfolio intake, risk classification, fund mapping, trading authority, contribution behavior, and support tools. Fidelity Go is built around a proprietary risk-scoring and discretionary management model. Acorns is built around Modern Portfolio Theory allocation, user-driven funding behavior, and automation that changes how regularly small amounts get invested.

The Return Comparison Is a Poor Proxy for the Automation Model

A return table answers a narrow question: what happened over a defined period for a defined account type or model. It does not answer who had discretion, what algorithm classified the investor, what instruments implemented the allocation, or whether the system was changing the investor’s behavior outside the portfolio engine. Those distinctions are especially important when a lawyer is reviewing a platform for a benefits context, employee financial wellness program, or internal recommendation policy.

Fidelity’s program legal booklet is unusually important here because it describes the machinery rather than just the app experience. Fidelity Go uses a proprietary methodology to assign an investor a risk score from 1 to 10, maps that score into one of 16 portfolios, and delegates discretionary trading authority to Strategic Advisers LLC.[2] That is not merely “an algorithm suggests a portfolio.” It is a managed account arrangement in which the adviser has authority to trade within the program’s disclosed framework.

Acorns describes its investment approach differently. Its educational material presents the robo-advisor model as Modern Portfolio Theory-based allocation across diversified portfolios, with user answers helping determine the recommended portfolio.[3] The automation around Acorns also includes features that are not portfolio construction in the strict sense: recurring deposits, Round-Ups, and other nudges that change funding behavior. That may sound less technical than a proprietary 1–10 score, but for many small-balance investors, the larger practical effect may be whether money enters the account at all.

| Question | Fidelity Go | Acorns |

|---|---|---|

| What does the core algorithm do? | Scores risk on a proprietary 1–10 scale and maps the investor to one of 16 portfolios. | Uses Modern Portfolio Theory-based allocation to place the investor in one of five risk portfolios. |

| Who trades the account? | Strategic Advisers LLC has discretionary trading authority within the program. | The platform recommends and automates funding behavior, but the user’s funding choices remain central. |

| What implements the portfolio? | Fidelity Flex mutual funds with 0% expense ratios. | iShares ETFs with disclosed expense ratios in the 0.04%–0.22% range. |

| Where does “AI” or automation show up most visibly? | Risk scoring, portfolio mapping, daily monitoring, and discretionary trading. | Portfolio allocation, Round-Ups, recurring behavior, and an AI chatbot disclosed for financial literacy support. |

| What should a legal reviewer read first? | The program legal booklet. | Pricing disclosures, investment methodology materials, and privacy disclosures. |

Fidelity Go: Proprietary Scoring Plus Delegated Trading Authority

The cleanest way to understand Fidelity Go is to follow the decision path. The investor answers intake questions. Fidelity’s methodology converts those answers into a risk score from 1 to 10. That score is associated with one of 16 model portfolios. Strategic Advisers LLC then manages the account on a discretionary basis, including daily trading activity as described in the program materials.[2]

That discretionary point should not be glossed over. In a legal review, it is different from a tool that merely displays an allocation and waits for the user to implement it. The investor is not approving each rebalance trade one by one. The program booklet identifies Strategic Advisers LLC as the party making and executing those trading decisions within the agreed program authority.[2]

The implementation is also distinctive. Fidelity Go portfolios use Fidelity Flex mutual funds, which carry 0% expense ratios.[2] That does not make the service costless at every balance level, but it separates fund expense from advisory pricing more clearly than a model built with third-party ETFs. Fidelity’s own overview states a $0 account minimum, a 0% advisory fee below $25,000, a 0.35% advisory fee at $25,000 and above, and unlimited 30-minute coaching calls once the account reaches the $25,000 threshold.[4]

The coaching feature is easy to overread. It adds human access, but it does not convert every algorithmic trade into a bespoke lawyerly consultation between investor and adviser. For comparison purposes, it matters because it marks where a human professional appears in the service design: not as the person approving every rebalance, but as a resource available at the stated balance tier.

Tax-loss harvesting is the one Fidelity Go feature that deserves a caution label. Fidelity’s own FAQ says tax-loss harvesting is available for taxable accounts at $25,000 and above.[5] Some third-party reviews have described the feature differently, which may reflect timing, product changes, or review methodology rather than a clean factual disagreement. For a legal or compliance review, Fidelity’s current primary disclosure should carry more weight than a summary review, but the inconsistency is exactly the kind of feature-level risk that should be checked again before relying on it.

Acorns: MPT Allocation Wrapped in Behavioral Automation

Acorns begins with a more familiar robo-advisor structure: the user answers questions, the system recommends a portfolio, and the allocation is grounded in Modern Portfolio Theory.[3] The available materials identify five risk portfolios implemented with iShares ETFs, whose expense ratios fall between 0.04% and 0.22%. That is a different architecture from Fidelity’s 16-portfolio Flex fund structure, not just a different brand name for the same engine.

The more interesting Acorns automation is not necessarily inside the portfolio optimizer. It is in the funding workflow. Round-Ups turn ordinary spending into an investing prompt by rounding purchases and investing the difference under the user’s settings. Acorns reported that Round-Ups averaged $45 per month per participating customer in July 2025 internal data.[6] That number should not be treated as an independent effectiveness study, but it does show what Acorns is trying to automate: not only asset allocation, but repeated investor action.

That distinction matters because an elegant portfolio that receives no deposits is mostly theoretical. Acorns’s design makes funding behavior part of the product. A lawyer reviewing the platform should not dismiss Round-Ups as a gimmick merely because it is not a sophisticated risk model. It changes when money moves, how often the user notices the account, and how the user experiences investing as a background activity rather than a separate financial chore.

Acorns’s pricing is subscription-based rather than asset-based. The disclosed tiers are $3, $6, and $12 per month.[7] That structure can be favorable or unfavorable depending on account size. A flat monthly subscription may be simple to explain, but on a very small account it can represent a high effective annual cost. On a larger account, the same flat charge may look modest compared with an assets-under-management fee.

The IRA match is another feature where the headline can move faster than the conditions. Available materials identify a 1% match on the Silver tier and a 3% match on the Gold tier, limited to first-year contributions and subject to a four-year holding requirement. For someone staying in the product long enough to satisfy the condition, it may affect the economics. For a short planning horizon, it should not be counted as immediately equivalent to cash.

Where the AI Label Actually Belongs

The phrase “AI robo-advisor” can obscure more than it explains. Fidelity Go’s primary disclosed automation is not a chatbot deciding what a user should buy. It is a scoring, mapping, monitoring, and trading process inside a regulated advisory program. The legal significance comes from discretionary authority, adviser status, portfolio implementation, and the documents that bind the arrangement.

Acorns places more of the visible automation around the investing workflow. Its privacy policy discloses an AI chatbot for financial literacy support, accessed in March 2026, but that disclosure should not be confused with proof that the chatbot is managing portfolios or exercising trading discretion.[8] The chatbot belongs in the support and education layer unless Acorns’s disclosures say otherwise.

For legal professionals, this is the central separation: portfolio-construction logic, discretionary trading authority, behavioral automation, and educational AI are different things. Putting them all under the same “AI” label makes the product easier to market and harder to review.

Fiduciary Status Does Not Make the Platforms Operationally Equivalent

Both platforms are described in the research materials as SEC-registered investment advisers owing fiduciary duties under the Investment Advisers Act of 1940. That shared regulatory baseline matters, but it does not collapse the operational differences. A fiduciary adviser with discretionary trading authority presents a different review question than a platform where the user’s funding behavior and subscription economics carry more of the practical weight.

The better review sequence is therefore not fee first, app second, performance third. It is authority first: who can trade, under what authorization, using what model, implemented through which instruments, and disclosed in which controlling document. Fees then become part of the same analysis rather than a substitute for it.

| Review point | Why it matters |

|---|---|

| Delegated discretion | Determines whether the adviser can trade without transaction-by-transaction user approval. |

| Risk scoring or portfolio mapping | Shows how the user’s answers become a portfolio assignment. |

| Investment implementation | Separates proprietary mutual fund architecture from third-party ETF architecture. |

| Behavioral automation | Identifies whether the platform is shaping deposits and user habits, not just allocation. |

| Feature-source hierarchy | Gives priority to program booklets, FAQs, pricing pages, and privacy policies over generalized reviews. |

The Practical Comparison

Fidelity Go is the cleaner fit for a reviewer who wants a documented advisory mechanism: proprietary risk score, 16 portfolios, Fidelity Flex funds, discretionary trading by Strategic Advisers LLC, and a clear asset-based fee breakpoint.[2][4] Its weakness is not opacity at the architecture level; the larger caution is feature verification, especially around tax-loss harvesting, because secondary sources have not described it consistently.[5]

Acorns is the stronger example of automation as behavior design. Its MPT-based five-portfolio model is simpler to describe, while Round-Ups and subscription tiers make the economics depend heavily on account size and user behavior.[3][6][7] Its AI chatbot disclosure belongs in the literacy and support layer, not in the portfolio-management layer unless later disclosures say more.[8]

The 2024 return comparison does not justify treating the platforms as interchangeable. It does the opposite. When the returns are nearly identical over one reported period, the meaningful differences are the ones ordinary comparison charts tend to compress: fee structure, delegated discretion, fund architecture, behavioral automation, and the reliability of the source describing each feature.

References

- 2024 Robo-Advisor Performance, Condor Capital Wealth Management via Investopedia.

- Fidelity Go Program Fundamentals, Fidelity.

- What Is a Robo-Advisor?, Acorns.

- Fidelity Go, Fidelity.

- Fidelity Go FAQs, Fidelity.

- Round-Ups, Acorns, July 2025 internal data.

- Pricing, Acorns.

- Privacy Policy, Acorns, accessed March 2026.

Comments

Join the discussion with an anonymous comment.